Ali

Ali Est. reading time:

Est. reading time:

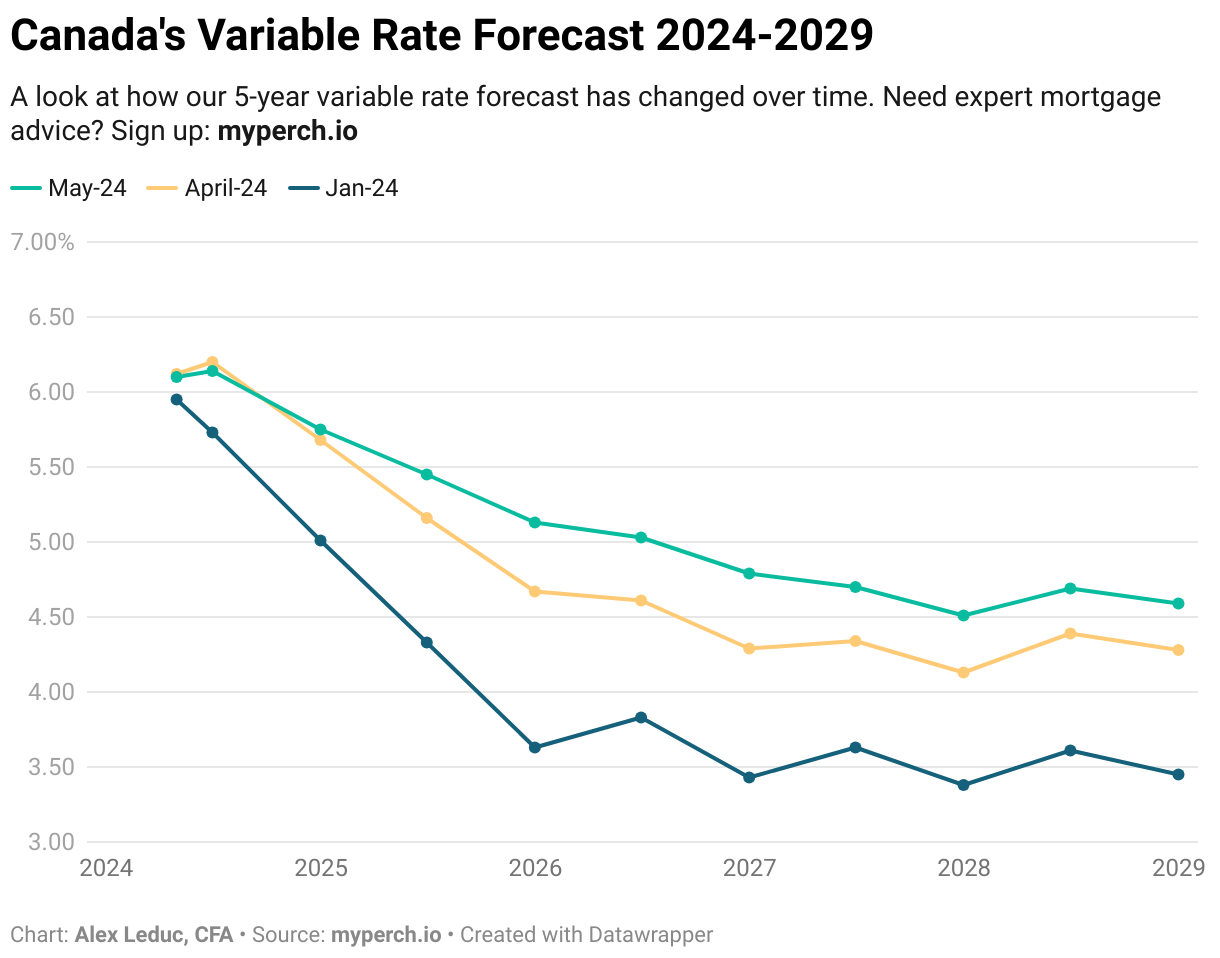

Read the June 2023 Canada interest rate forecast.

Read the August 2023 Canada interest rate forecast

Following the latest interest rate hike on June 7th from the Bank of Canada, analysts are wondering if we have more rate hikes in store for 2023. While recent data has shown that inflation is slowing and the CPI is getting closer and closer to the Bank of Canada’s target, some are predicting we may have one more rate hike on the way before another pause. After a 25bps increase in January the Bank of Canada paused rates to evaluate the effect that hikes were having on inflation, and then resumed tightening monetary policy with another 25bps hike in June. The next interest rate announcement from the Bank of Canada is on July 12th 2023 and while there’s no guarantee on the outcome, we’re predicting we’ll see at least one more rate hike before 2023 is over, followed by an eventual reversal of policy.

Key Takeaways

- Bank of Canada has resumed tightening monetary policy, and raised interest rates by 0.25% in June.

- For buyers, there are great opportunities in the market, but inventory is low across the board.

- Today’s best mortgage rates are 4.97% for 5-year fixed and 5.85% on 5-year variable.

- For homeowners coming up for renewal, continue to monitor our rate forecast and avoid taking the first offer from your existing lender, as they’re typically less competitive.

Here’s how the mortgage market is doing going into July:

For the month of July, we anticipate fixed rates will increase slightly and variable rates might increase on the back of a potential 25 bp rate hike by the Bank of Canada. National sales activity continues to rise in May but at a slower pace (+5.1%), following April’s double digit growth (+11.3%). Keeping in trend for 2023, the number of new supply has increased by 6.8% month over month, this is typical for Spring market activity, however supply remains historically low across all major markets. Monthly sales activity is now heading towards the pre-pandemic 10 year moving average, with 3.1 months of inventory, a month over month decline of .2. The Aggregate Composite MLS Home Price Index made another jump of 2.1% on a month-over-month basis in May, a notable increase from 1.6% in April. The tale of the market is buyer demand continues to outweigh supply, keeping us in a Seller favored market. We anticipate a more balanced market as we head deep into the summer months, where more supply will enter the market and buyer demand will begin to taper off as higher interest rates slow down purchasing power.

Will the bank of Canada continue raising rates?

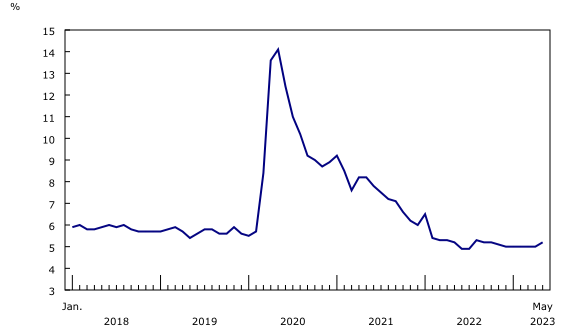

Higher than anticipated April CPI inflation numbers (+4.4%) and positive first quarter GDP results (+0.8%) sent markets in a new trajectory as all was certain the Bank of Canada would raise its key lending rate by 25 basis points in June, for the first time since January. The Bank of Canada increased their key lending rate to 4.75%, according to the Central Bank, this was necessary based on “evidence that points to excess demand in the economy persisting longer than expected, increasing the risk that inflation could get stuck above the 2% target.” With markets having largely priced in a further rate hike in the coming months, there is a growing consensus the Bank of Canada might choose to pause and assess against a backdrop of cooling inflation and emerging stress cracks in the banking and commercial real estate sectors. With only 3 more meetings set for 2023 thereafter, we anticipate the Bank will close off the year at a 5% policy rate, keeping in line with our neighbors down south.

GDP growth remains lower than inflation.

April GDP data released on June 30th shows that growth stalled, remaining essentially unchanged and coming in below expectations, while this may be welcomed data by the BoC, preliminary May data suggest GDP expanded .4%. The real estate and rental leasing sector grew (+.5%) for the sixth consecutive month on the back of heightened re-sale activity in the first 3 months of 2023, the sector’s largest growth since December 2020. Statistics Canada’ June report shows the Canadian economy continues to move against expectations of an incoming slowdown in Q2, now expected to expand by 1.4%, where the central bank had set expectations for 1% growth. Following interest rate hikes from the Bank of Canada, which are meant to slow the economy, it’s inevitable that GDP growth will slow in the short term, the question remains: by how much? The Bank of Canada is currently hoping for a “soft landing” leading to a minor recession.

Key Terms:

GDP: GDP or Gross Domestic Product refers to the total dollar amount of goods and services produced in a country. It is an overall measure of the strength of our economy.

CPI: The CPI or Consumer Price Index is a measure of inflation tracked by Statistics Canada. It attempts to track the spending habits of the average consumer with a basket of typical goods and services.

Is inflation slowing down?

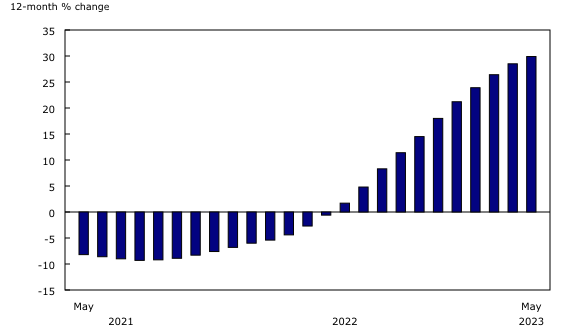

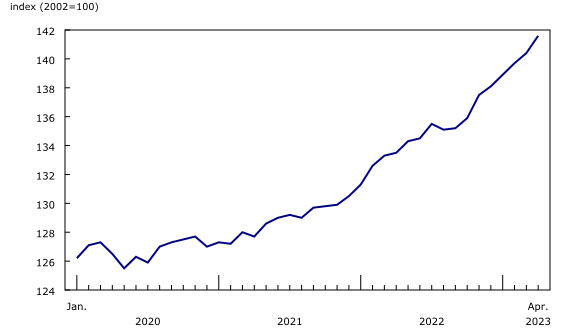

May’s consumer price index, the measure for year over year inflation, came in at +3.4%. After an increase in April of +0.1%, the BoC sounded the alarms that inflation is heading in the wrong direction and was convinced that there is more work to be done to reach the anticipated inflation targets for 2023. We’re now half way through the most difficult year for Canadians in recent history and inflation is nearly at the 2% target, when excluding mortgage interest cost (2.5%). The May CPI report indicates that the year over year slow down was mainly driven by lower gas prices (-18.3%) due to the 2022 base year effect when we saw energy costs surge across the board. Rising mortgage interest rates continue to apply the highest upward pressure on the CPI. Canadians shopping for a new home or renewing their mortgage in May experienced a staggering 29.9% increase in mortgage costs, the largest increase on record. We expect the CPI to continue to decelerate in June to 3% and trend closely to the Central Bank’s target of 2%, of course, when not accounting for mortgage interest cost. Tiff and the Bank of Canada must deliver a convincing monetary policy report come July 12th for the case to continue hiking their policy rate.

Unemployment is finally on the rise.

Stats Canada reported that Job vacancies edged down further in April, making it -8.4% year to date, and -21.2% since the all-time high reported vacancies reached in May 2022 . Unemployment rate has ticked upwards by .2% in May (5.2%), the first movement since August 2022, this was led by job decreases in Ontario, Nova Scotia and Newfoundland and Labrador in, all other provinces recorded little change.

Canada’s population hit 40 million for the first time.

Canada’s population is growing, at a fast rate, and has officially joined the 40 million club! While the Central Bank continues to warn that strong population growth is supporting aggregate consumption and employment growth, the Federal Government is marching full steam ahead with their goal of 1.4 million new immigrants in the next 3 years. Canada welcomed 145,417 immigrants in the first quarter of 2023 alone, a new record, many of those arriving in Canada’s major markets are searching for shelter amidst the home unaffordability crisis, driving up rental cost (+6.5%) in May, culprit, high demand, low supply and landlords facing negative cash flow due to recent rate hikes on their investment homes.

Recommended reading: How does population affect the housing market?

Bonds trend higher

Bond yields continue to rise, at a faster rate and to levels not seen since late 2007. The month of June continued on the back of a 70 basis point increase in May, with yields increasing by a further 45 basis points since the beginning of the month. Yields are increasing as core CPI stagnates, mortgage cost index continues to rise, GDP growth remains positive and tight labour market conditions have convinced markets the central bank has no option but to continue to hike their rate. Canadian markets continued to react negatively to hawkish commentary by the Fed speaker Jerome Powell and the BoC’s very own, Tiff Macklem, on their commitment to increase their key rates, even at the cost of completely stalling the economy and plunging them into a recession.

If you’re looking to buy a home in Canada:

Our current best 5-year fixed rates are 4.97% and 5-year variable rate of 5.85%.

For first-time home buyers, there are some great opportunities outside of core markets, sellers are coming to terms with tapering price growth as higher interest rates bar many from entering the market, however, inventory is still at record lows, so we’re not at a balanced market quite yet.

For homeowners who are coming up for renewal, continue to monitor our rate forecasts, it would be wise to see what rates Perch may be able to offer above and beyond your existing Lender, as they’re typically less aggressive on their rate offerings.

For homeowners who would like to see the benefit of switching lenders and breaking their mortgage early, Perch automatically calculates the net benefit once you input your existing property and mortgage details in your Perch portfolio.