Ali

Ali Est. reading time:

Est. reading time:

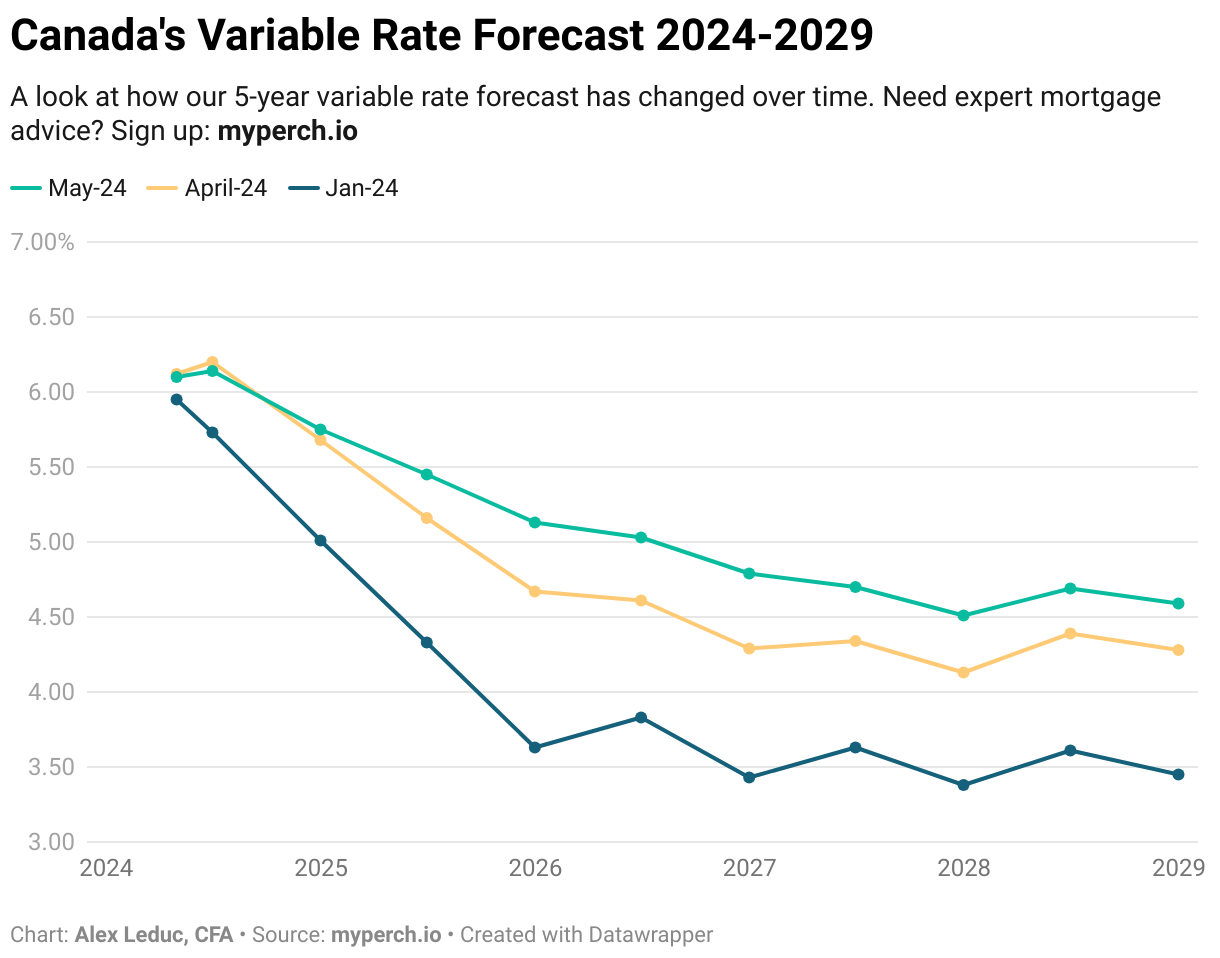

Read the July 2023 Canada interest rate forecast.

Read the September 2023 Canada interest rate forecast.

The Bank of Canada hiked interest rates by another 0.25 basis points in July, bringing the key rate to 5.00%. Recent data has shown that inflation is slowing and the CPI is getting closer and closer to the Bank of Canada’s target, leading to some analysts predicting that the Bank of Canada might hold off on further rate hikes for the time being. After a 25bps increase in January the Bank of Canada paused rates to evaluate the effect that hikes were having on inflation, and then resumed tightening monetary policy with another 25bps hike in June. This pause indicates the Bank of Canada think the effect of their rate hikes may be getting close to bringing inflation back in line to their target of 2.00%. The next interest rate announcement from the Bank of Canada is on September 6. Whether the Bank of Canada decides to hold rates at their current level or increase the policy interest rate one more time, it’s seeming more likely that we’re nearing the end of rate hikes in the short term as CPI continues to slow.

Key Takeaways

- The Bank of Canada has continued tightening monetary policy, and raised interest rates once again by 0.25% in July.

- For buyers, there are great opportunities in the market, but inventory is low across the board.

- Today’s best mortgage rates are 5.17% for 5-year fixed and 6.10% for 5-year variable.

- For homeowners coming up for renewal, continue to monitor our rate forecast and avoid taking the first offer from your existing lender, as they’re typically less competitive.

Here’s how the mortgage market is doing going into August:

For the month of August, we anticipate fixed rates will increase slightly and variable will remain the same. National sales activity continued to edge up in June but at a slower pace (+1.50%), following May’s (+5.10%) and April’s double digit growth (+11.30%). June’s number of actual of transactions was 4.70%, when not seasonally adjusted, a number we haven’t seen in the last 2 years. The number of new supply has increased by 5.90% month over month, recovering from 20 year lows and heading towards average number territory, “With sales levelling off near historically average levels and new listings finally starting to play catch up, housing markets appear to be settling down,” said Shaun Cathcart, CREA’s Senior Economist. The Aggregate Composite MLS Home Price Index made another jump of 2.00% on a month-over-month basis in June, slightly lower than May’s 2.10% increase, signaling we might’ve now seen the top of the market and heading towards expected lower home prices as both higher interest rates and more inventory apply downward pressure on pricing across Canada. The actual (not seasonally adjusted) national average home price was $709,218 in June 2023, up 6.70% years over year.

The Bank of Canada increased interest rates once again in July

The Bank of Canada increased their key lending rate by 25 basis points, bringing it to 5.00% as of July. According to the Central Bank, this was necessary based on evidence that points to excess demand in the economy persisting longer than expected, which may jeopardize their efforts to bring down inflation to the 2.00% target. Markets and Senior Economists are largely divided on whether anymore further rate hikes may be necessary, according to the Bank of Canada’s annual survey of Canadian Economists, there is a growing consensus that the Central Bank should pause and assess against a backdrop of cooling inflation (2.8% in July) and early signs of a contracting economy in the upcoming 6 months. With only 3 more meetings set for 2023, we anticipate the Bank will close off the year at a 5.00% policy rate.

GDP growth remains lower than inflation.

April GDP data released on June 30th shows that growth stalled, remaining essentially unchanged and coming in below expectations, while this may be welcomed data by the BoC, preliminary May data suggest GDP expanded .40%. The real estate and rental leasing sector grew (+.50%) for the sixth consecutive month on the back of heightened re-sale activity in the first 3 months of 2023, the sector’s largest growth since December 2020. Statistics Canada’ June report shows the Canadian economy continues to move against expectations of an incoming slowdown in Q2, now expected to expand by 1.40%, where the central bank had set expectations for 1.00% growth. Following interest rate hikes from the Bank of Canada, which are meant to slow the economy, it’s inevitable that GDP growth will slow in the short term, the question remains: by how much? The Bank of Canada is currently hoping for a “soft landing” leading to a minor recession.

Key Terms:

GDP: GDP or Gross Domestic Product refers to the total dollar amount of goods and services produced in a country. It is an overall measure of the strength of our economy.

CPI: The CPI or Consumer Price Index is a measure of inflation tracked by Statistics Canada. It attempts to track the spending habits of the average consumer with a basket of typical goods and services.

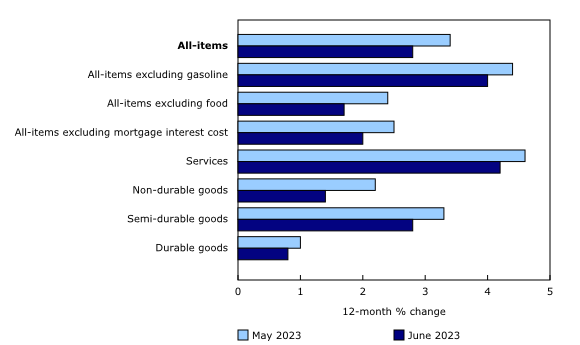

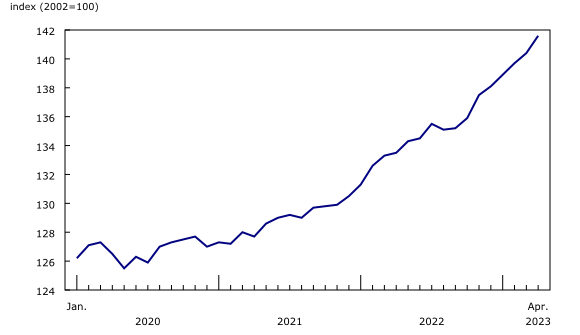

CPI slows in June, bringing inflation closer to the Bank of Canada’s target

June’s consumer price index, the measure for year over year inflation, came in at +2.00%, when excluding mortgage interest cost, +2.80% actual, following a 3.40% year over year increase in May. June’s CPI declaration was largely in part due to a year over year decline in the price of Oil, the CPI in June was +4.00% when excluding gasoline, Canadians paid 21.60% less at the pump versus June 2022, however this is due to the base year effect, when Oil prices had reached new heights. With now 6 months of 2023 inflation data available, and a decrease of 3.10% from January’s +5.90% all item’s CPI, early estimates indicate that we will see the CPI tick upwards, signaling an unwelcomed reverse in direction as Canadians continue to battle elevated grocery prices (+9.10%) and mortgage interest costs (+30.10%) in June and beyond. Rising mortgage interest rates continue to apply the highest upward pressure on the CPI, making up 40.00% of topline inflation. Canadians shopping for a new home or renewing their mortgage in June experienced a staggering 30.10% increase in mortgage costs, the largest increase on record. We expect the CPI to continue to hold near the 2.00% mark in July when the numbers are released, of course, when not accounting for mortgage interest cost.

Canada’s job market continues to grow

Canada added 60,000 new jobs in April, mostly full time jobs, the largest increase since January, once again, passing expectations. Job vacancies continued to trend downward in May (-3.30%) as they have been for the past year, there were 1.4 unemployed persons for each job vacancy, up from the low of 1.0 recorded in June of 2022.

Unemployment rises to highest level since February 2022

The unemployment rate rose a further 0.2 percentage points to 5.40%, the second increase since August 2022 and highest it has been since February 2022. Wage growth is showing signs of stalling as average hourly wages rose 4.2% in June, the lowest year over year increase since May of 2022.

Canada’s population continues to grow, adding demand

Canada’s population is rapidly growing and recently passed 40 million for the first time last month. The Bank of Canada continues to warn that strong population growth is supporting aggregate consumption and employment growth, “Strong population growth from immigration is adding both demand and supply to the economy: newcomers are helping to ease the shortage of workers while also boosting consumer spending and adding to demand for housing” according to the Bank of Canada’s July Monetary Policy Report. Canada welcomed 145,417 immigrants in the first quarter of 2023 alone, a new record, many of those arriving in Canada’s major markets are searching for shelter amidst the home unaffordability crisis, driving up rental cost (+6.50%) in May, culprit, high demand, low supply and landlords facing negative cash flow due to recent rate hikes on their investment homes.

Recommended reading: How does population affect the housing market?

Bond yields continue to rise

Bond yields continue to rise, at a faster rate and to levels not seen since late 2007. The month of July saw Canada’s 5 year bond yield breach the 4.00% ceiling, then retreating, on the back of a 100 basis point increase since May. Yields are increasing mainly as stronger than anticipated job reports, core CPI showing signs of stagnation, mortgage cost index continuing to rise and positive GDP growth have convinced markets the central bank has no option but to continue to hike their rate, or they may hold higher interest rates for longer. The Bank of Canada remains resolute in their mission to battle inflation, even at the cost of completely stalling the economy and plunging Canada into a recession.

If you’re looking to buy a home in Canada:

Our current best 5-year fixed rates is 5.17% and 5-year variable rate of 6.10%.

For first-time home buyers, there are some great opportunities outside of core markets, sellers are coming to terms with tapering price growth as higher interest rates bar many from entering the market, however, inventory is still low, so we’re not at a balanced market quite yet.

For homeowners who are coming up for renewal, continue to monitor our rate forecasts, it would be wise to see what rates Perch may be able to offer above and beyond your existing Lender, as they’re typically less aggressive on their rate offerings.

For homeowners who would like to see the benefit of switching lenders and breaking their mortgage early, Perch automatically calculates the net benefit once you input your existing property and mortgage details in your Perch portfolio.