Ali

Ali Est. reading time:

Est. reading time:

Read the August 2023 Canada interest rate forecast.

The Bank of Canada hiked interest rates by another 0.25 basis points in July, bringing the key rate to 5.00%. With the next interest rate announcement due on September 6th, most analysts are predicting the Bank of Canada will hold the key rate steady. Whether the Bank of Canada decides to hold rates at their current level or increase the policy interest rate one more time, it’s seeming more likely that we’re nearing the end of rate hikes in the short term as CPI continues to slow.

Key Takeaways

- The last rate hike was on July 12th bringing the key rate to 5.00%.

- The next interest rate announcement will be on September 6th and most analysts are predicted rates will remain unchanged.

- For buyers, there are great opportunities in the market, but inventory is low across the board.

- Today’s best mortgage rates are 5.44% for 5-year fixed and 5.95% for 5-year variable.

- For homeowners coming up for renewal, continue to monitor our rate forecast and avoid taking the first offer from your existing lender, as they’re typically less competitive.

Here’s how the mortgage market is doing going into September:

For the month of September, we anticipate fixed rates will stagnate while variable rates could increase, should the Bank of Canada increase it’s key lending rate on September 6th. National sales activity edged down in July by 0.7% month over month, remaining on trend with June’s declining sales activity. July’s number of actual of transactions was 8.7%, when not seasonally adjusted, the largest we’ve seen in the last 2 years. The number of new supply has been steadily increasing, for the month of July, Canada’s inventory increased by 5.6% month over month, recovering from 20 year lows earlier this year and quickly heading towards average number territory. When sales activity begins to taper off and inventory continues to increase, buyers are left with more options, leading to lower price growth, not to mention, increased speculation of when and if the housing market might bottom out. “Sales and price growth are already showing signs of tapering off further in August in response to the Bank of Canada’s mid-July rate hike and messaging regarding above-target inflation for longer than previously expected. We’re probably looking at another round of ʻback to the sidelines’ for some buyers until there’s a higher level of certainty around interest rates going forward.” said Shaun Cathcart, CREA’s Senior Economist.

The Aggregate Composite MLS Home Price Index climbed by a further 1.1% on a month-over-month basis in July, lower than June’s 2% increase, signaling we might’ve now seen the top of the market and heading towards expected moderating home prices as both higher interest rates and increased inventory apply downward pressure on pricing nationally. The actual (not seasonally adjusted) national average home price was $668,754 in July, up 6.3% years over year.

The next Bank of Canada rate announcement is scheduled for September 6th

The Bank of Canada increased their key lending rate by 25 basis points, bringing it to 5.00% during the last interest rate announcement in July. September 6th will mark a crucial date as The Bank of Canada decides whether to increase their key lending rate by 25 basis points, as they did in July, or choose to pause and assess. With only 2 more meetings set for 2023 thereafter, we anticipate the Bank will close off the year at a 5.25% policy rate should they choose to increase their key lending rate. While the Central Bank believes there’s substantial evidence pointing to excess demand in the economy persisting longer than expected, markets and Senior Economists are largely divided on whether anymore further rate hikes may be necessary to curb inflation, which has already declined to levels below those anticipated, and are only back on the rise mainly due to increased mortgage costs and price of gasoline. The Bank of Canada has a softening labour report and a GDP report to consider before their next meeting, whichever route the Bank of Canada decides to take, Canadians will be facing higher cost of everything a little longer than anticipated, as inflation is not expected to subside to the needed 2% levels until late 2024.

Strength of the economy

April GDP data released on June 30th shows that growth stalled, remaining essentially unchanged and coming in below expectations, while this may be welcomed data by the BoC, preliminary May data suggest GDP expanded .40%. The real estate and rental leasing sector grew (+.50%) for the sixth consecutive month on the back of heightened re-sale activity in the first 3 months of 2023, the sector’s largest growth since December 2020. Statistics Canada’ June report shows the Canadian economy continues to move against expectations of an incoming slowdown in Q2, now expected to expand by 1.40%, where the central bank had set expectations for 1.00% growth. Following interest rate hikes from the Bank of Canada, which are meant to slow the economy, it’s inevitable that GDP growth will slow in the short term, the question remains: by how much? The Bank of Canada is currently hoping for a “soft landing” leading to a minor recession.

Key Terms:

GDP: GDP or Gross Domestic Product refers to the total dollar amount of goods and services produced in a country. It is an overall measure of the strength of our economy.

CPI: The CPI or Consumer Price Index is a measure of inflation tracked by Statistics Canada. It attempts to track the spending habits of the average consumer with a basket of typical goods and services.

Inflation continues to slow over the summer

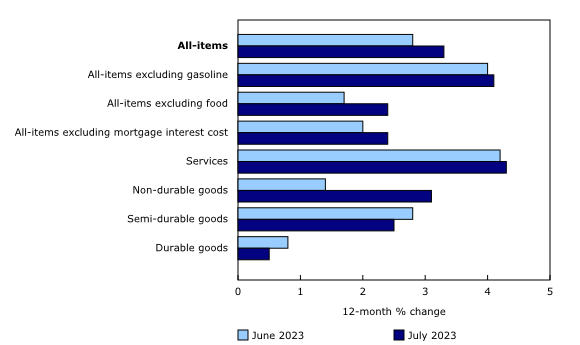

July’s consumer price index, the measure for year over year inflation, came in at +2.4%, when excluding mortgage interest cost, +3.3% actual, following a 2.8% year over year increase in June. As anticipated, July’s increase came mainly as a result of gasoline prices base-year effect, with now early estimates confirming we will see the CPI continue to tick further upwards in August and beyond, as the Bank of Canada treads on their monetary policy of fighting fire with fire. Canadians continue to battle elevated grocery prices (+8.5%) and mortgage interest costs (+30.6%) in July and beyond, notably, mortgage interest rates continue to apply the highest upward pressure on the CPI, making up 37.5% of topline inflation. The Central Bank sees tightening household discretionary spending as their most viable tool to halt consumer spending on goods and services, and attain their 2% inflation target.

Canadians shopping for a new home or renewing their mortgage in July experienced a staggering 30.6% increase in mortgage costs, the largest increase on record. We expect the CPI to continue to hold near the 2% mark in July, of course, when not accounting for mortgage interest cost.

The job market shrunk for a change

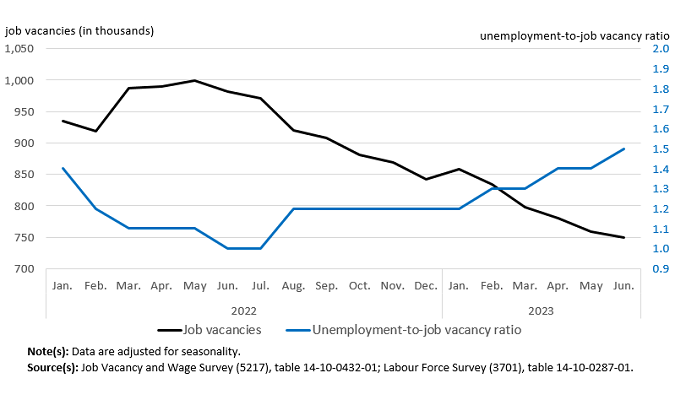

The labour market is marking a turn of events, Canada shed 6,400 jobs July, vs expectations of an increase of 25,000 new jobs. July’s report shows the slowing labour market’s softening was lead by the construction sector (-45,000) and offset by growth in health care and social assistance (+25,000), educational services (+19,000), finance, insurance, real estate, rental and leasing (+15,000) and agriculture (+12,000).

Job vacancies continued to trend downward to their lowest since May of 2021, this is on trend for the past 12 months, edging down by 8,900 (-1.2%) to 753,400 in June, following May’s decline (-3.3%) a further sign indicating the labour market tightness has eased.

The unemployment rate rose a further 0.1 percentage points to 5.5%, the third consecutive increase since August 2022 and the highest it has been since February 2022. This data will be welcomed by the Bank of Canada as they’ve repeatedly indicated the labour market’s softening as a key metric on their quest to tame inflation.

Canada’s population continues to grow, outpacing new housing supply

The Bank of Canada continues to warn that strong population growth is supporting aggregate consumption and employment growth, according to their July Monetary Policy Report, “Strong population growth from immigration is adding both demand and supply to the economy: newcomers are helping to ease the shortage of workers while also boosting consumer spending and adding to demand for housing.” Ottawa plans to accept 465,000 permanent residents into the country in 2023, with the immigration target growing to 500,000 in 2025. Many of those arriving in Canada’s major markets are searching for shelter amidst the home unaffordability crisis, driving up rental cost (+8.9%) in July. Provinces rely heavily on Canadian investors to supply rental apartments in the form of investment homes, however, as higher interest rates and mortgage costs have worked to deter existing and would be landlords, the supply of rentals has steadily declined.

Recommended reading: How does population affect the housing market?

Bond yields on the rise again

Bond yields continued to rise, at a faster rate and to levels not seen since 2007. The month of August saw Canada’s 5-year bond yield breach the 4% ceiling and stay there, closing off the month 40 basis points below the peak we saw of 4.2%. Bond yields have increased more than a 100-basis point increase since May, primarily due to stronger than anticipated job reports, core CPI showing signs of stagnation, mortgage cost index continuing to rise and positive GDP growth having convinced markets the central bank is not done hiking their key rate, or they may hold higher interest rates for longer. The Bank of Canada remains resolute in their mission to battle inflation, even at the cost of completely stalling the economy and plunging Canada into a recession, an outcome that’s becoming extremely likely.

If you’re looking to buy a home in Canada:

Our current best 5-year fixed rates is 5.44% and 5-year variable rate of 5.95%.

For first-time home buyers, there are some great opportunities outside of core markets, sellers are coming to terms with tapering price growth as higher interest rates bar many from entering the market, however, inventory is still low, so we’re not at a balanced market quite yet.

For homeowners who are coming up for renewal, continue to monitor our rate forecasts, it would be wise to see what rates Perch may be able to offer above and beyond your existing Lender, as they’re typically less aggressive on their rate offerings.

For homeowners who would like to see the benefit of switching lenders and breaking their mortgage early, Perch automatically calculates the net benefit once you input your existing property and mortgage details in your Perch portfolio.