Ali

Ali Est. reading time:

Est. reading time:

Read the January 2023 Canada interest rate forecast.

Read the March 2023 Canada interest rate forecast.

Latest Mortgage Rate Outlook in Canada for February 2023

2023 started off on a painful note for holders of variable rate mortgages with the Bank of Canada announcing a 25 basis point increase for interest rates on January 23rd. On the bright side, analysts are predicting that this could be the first and last rate hike for the year as inflation is slowing and the Bank of Canada prepares to take a step back and evaluate the situation before increasing rates any further. Let’s take a look at how the mortgage market is trending going into February.

The Bank of Canada announces another rate hike in January

For the 8th consecutive time, on January 25th, 2023, the BoC raised its policy interest rate. It was the first time the bank only raised its key interest rate by 25 basis points since March 2, 2022 bringing the current policy interest rate to 4.5%. The next Bank of Canada meeting is slated for March 8, we will cover our forecast for the next meeting on our March report. For now, it seems hopeful that the Bank of Canada may keep rates unchanged.

How are mortgage rates trending?

For the month of February, we anticipate fixed rates will continue to drop, variable rates will remain the same as the next Bank of Canada meeting will fall on March 8. According to CREA, national sales activity was up 1.3% month-over-month in December, however, as anticipated in our December forecast, the number of newly listed homes declined by 6.4% month-over-month, cementing one of the lowest December new supply levels on record. We expect January sales data to continue to increase nationally, and while we will see an uptick in supply, it will still be a record low, year over year, as January 2022 was a scorching hot market.

If you’re wondering why variable rates are now trending higher than fixed rates check out this article for a more in depth overview.

The economy is still holding on…

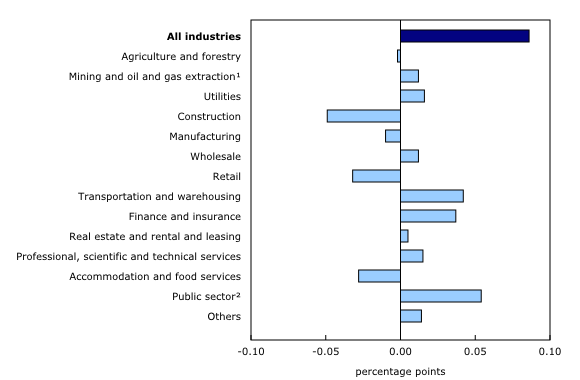

According to Statistics Canada, Real GDP edged up in November (0.1% month over month). Growth in services-producing industries (+0.2%) was partially offset by a decline in goods-producing industries (-0.1%), as 14 of 20 industrial sectors increased in November. According to Stats Canada advance information, real GDP remained unchanged in December. Q4 GDP data appears to be around 0.4%, an annual increase of 3.8% for 2022. The bank of Canada, in its January monetary policy report estimates GDP will grow by only 1% annually for 2023.

… but inflation is still relatively high

Following a 6.8% year over year increase in November, the Consumer Price Index (CPI) rose 6.3% year over year in the month of December. Excluding food and energy, prices increased 5.3% year over year. Rising mortgage interest rates continue to put upward pressure on the CPI, rising 18.0% year-over-year, following a 14.5% increase in November. The Bank of Canada has now revised it’s inflation outlook to 3% by mid 2023. We expect CPI to drop below 6% in the upcoming 21st of February release for the first time since February 2022 which would spell good news for the future of the housing market.

Canadians are working hard and the employment numbers reflect it

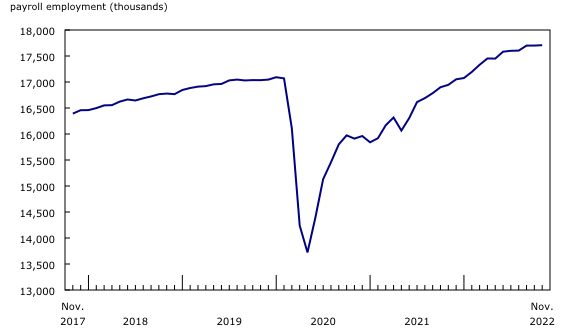

Declines in the job vacancy rate have been broad based, overall, the number of job vacancies across all sectors decreased by 2.4% in November, down from the highs recorded in May of 2022 and the lowest level recorded since August 2021. There were 1.2 unemployed persons for every job vacancy in November 2022, essentially unchanged since August, but up slightly from the low of 1.0 in June. Prior to the pandemic, the unemployment-to-job vacancy ratio hovered around 2.2.

In December, employment rose by 104,000, to put it into perspective, economists were expecting an increase of 5,000. The unemployment rate also declined by 0.1% month over month to 5.0%. This was the third decline in four months and left the rate just above the record low of 4.9% reached in July. The bank of Canada wants to see the unemployment rate trend higher and closer to 6% as a sign of a loosening labour market. When employment rates are high, there is more disposable income to go around which increases inflation. With that in mind, a higher rate of unemployment makes the Bank of Canada lowering interest rates more likely in the future

Wages are up across the board

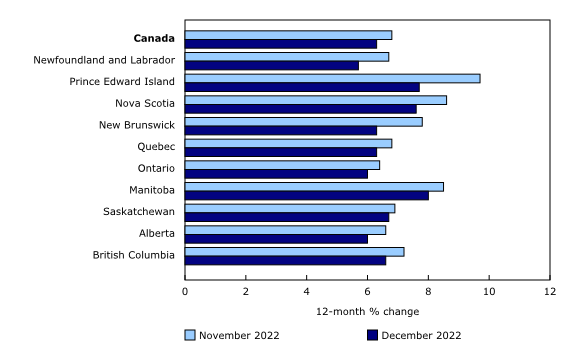

All provinces recorded year-over-year growth in average weekly earnings. Average weekly earnings grew 4.2% year-over-year in November, that’s .08% higher than October. Wage growth, an indicator of a tight labour market has been a sticking point for the BoC, who would like to see wage growth slow down and unemployment increase before letting off the gas pedal on rate hikes.

Canada’s population continues to grow

Canada’s population is growing faster than ever before, and it’s all thanks to immigration. According to Statistics Canada, as of October 2022, 362,453 people have immigrated to Canada since July 1, 2022, an increase of 0.9%, marking the highest quarterly population growth rate since the second quarter of 1957 (1.2%). While most of the third quarter population growth numbers were driven by an increase of 225,198 non-permanent residents who were already here on work permits, this increase in one quarter was larger than any full-year increase since 1971.

How are bond yields doing?

5-year bond yields bottomed at 2.79% mid January, yields not seen since August of 2022, with the 5-year bond yield hovering around 3%, lenders will be incentivized to decrease their 3 year and 5 year fixed rates to mid 4% throughout the month of February. We will finally begin seeing lower rates on short term fixed rates in 2023 as well.

Is now the right time to buy a home?

With rates possibly peaking and the housing market down across the board in cities, now might be the time to jump on the homeownership bandwagon if you’ve been waiting on the sidelines.

When interest rates eventually come down again it’s likely the increased demand will bring the housing market back to where it was pre 2022. If you go with a variable rate you could have the best of both worlds when rates come back down, or you could play it safe and go with a fixed rate mortgage.

Our current best 5-year fixed rate is 4.40% and a 5-year variable rate of 5.56%. For first-time home buyers, there are some great opportunities in a market dampened by negative sentiment and overall lack of competition.For homeowners who are coming up for renewal, rates are beginning to drop, continue to monitor our rate forecasts, it would be wise to renew into a one year terms until rates begin to decrease in the next year. For homeowners who would like to see the benefit of switching lenders and breaking their mortgage early, Perch automatically calculates the net benefit once you input your existing property and mortgage details in your Perch portfolio.