Ali

Ali Est. reading time:

Est. reading time:

Read November 2022 Canada interest rate forecast

Read January 2023 Canada interest rate forecast

Fixed rates close the gap with variable with rate increases soon to slow

For the month of December, we anticipate fixed rates to continue to drop, variable rates will increase slightly as the Bank of Canada increases its overnight lending rate, potentially for the final time in the near term. According to CREA, national sales activity edged a little higher in October (1.3% month over month). “Sales actually popped up from September to October, and the decline in prices on a month-to-month basis got smaller for the fourth month in a row,” said Shaun Cathcart, CREA’s Senior Economist. It will be interesting to observe whether November and December will follow in trend, as historically, there is lower inventory and motivated buyers as we head into the holiday season.

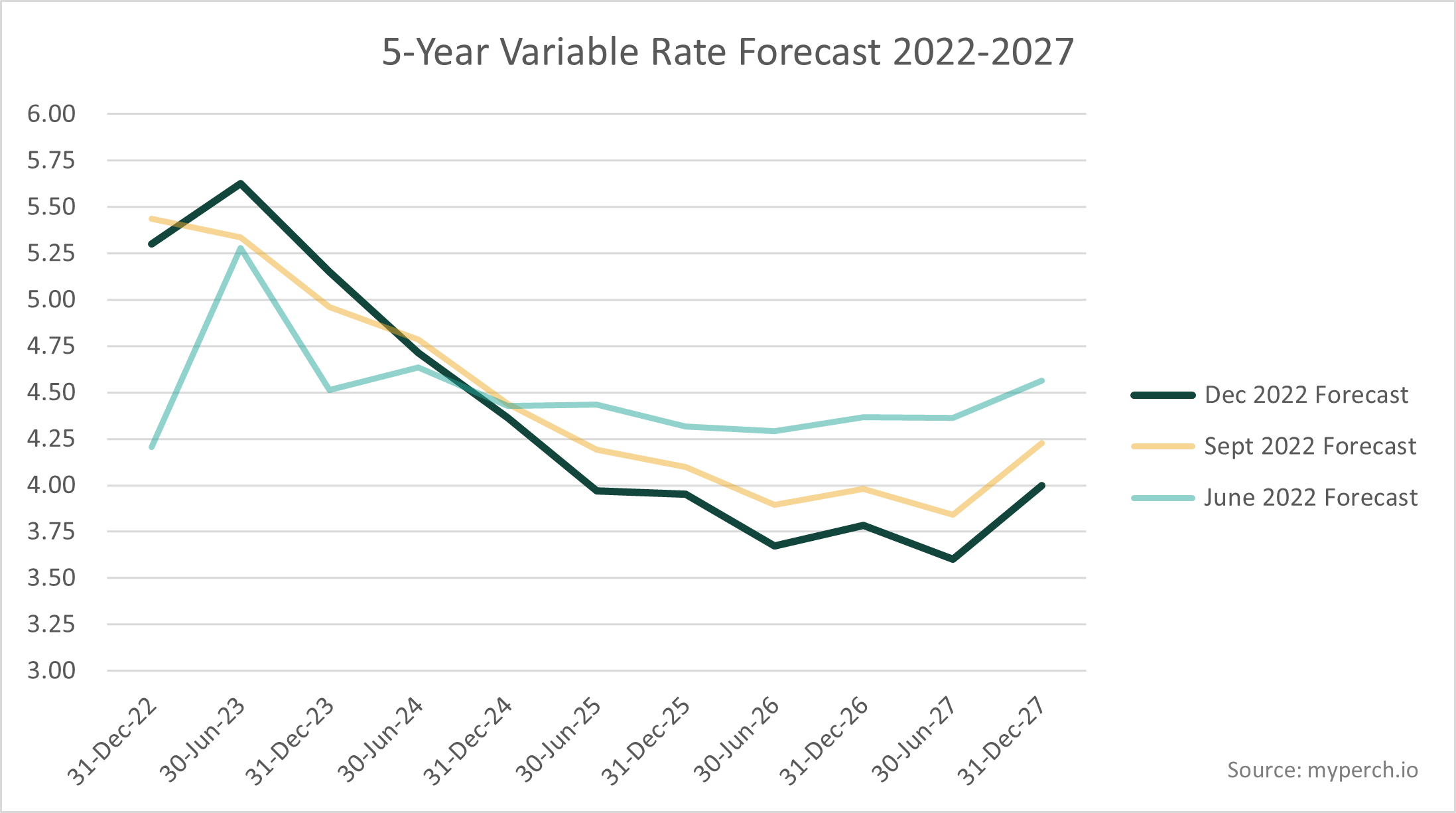

Based on our latest insights, here is Perch’s forecast for 5-year variable rate mortgages in Canada from 2022 to 2027. Relative to June 2022, accelerating inflation data has resulted in the Bank of Canada front loading more of the rate hikes instead of gradual increases. In later years (2025 and onwards), rates are expected to be roughly 0.50% lower than they were expected in June. The chart below displays how our forecast has changed over time, referencing the past two quarters.

Potentially one of the last rate hikes is on the way

The Bank of Canada announced its 7th straight rate hike, pushing the key interest rate up half a percentage point from 3.75% to 4.25%, on Wednesday, December 7th, 2022. Homeowners, investors and markets closely watched for the November 16 CPI numbers, inflation was up 6.9% year over year, matching September’s CPI. Tiff Macklem updated the House finance committee on the central bank’s balance sheet and answered an array of questions about the Bank’s plans for the coming year, “The Bank of Canada’s job is to ensure inflation is low, stable and predictable,” Macklem said. “We are still far from that goal. We view the risks around our forecast for inflation to be reasonably balanced. But with inflation so far above our target, we are particularly concerned about the upside risks.”

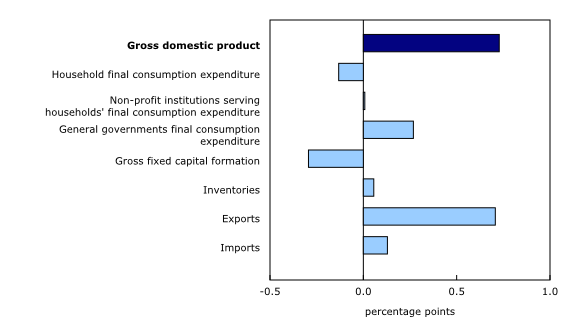

GDP rises slightly for the 5th quarter in a row

In the 3 quarter of 2022, GDP rose 0.7%, marking the fifth consecutive quarter with positive GDP growth. Stronger growth in exports, non-residential structures, and business investment in inventories were moderated by declines in housing investment and household spending. Housing investment accounted for about 8.2% of our GDP in Q3, a double digit drop from early 2021, and while GDP continues its positive trend, according to Statistics Canada, housing investment (-4.1%) declined for the second consecutive quarter, in part due to higher interest rates, renovation activity were also down (-6.6%) for the second consecutive quarter, and resale activities (-13.8%) were down for the third consecutive quarter.

Immigration is on the rise, how will this affect the rental market?

On November 1st, The federal Liberal government announced plans for an incremental increase in the number of immigrants entering Canada, 500,000 people each year by 2025. The Canadian government is seeking to address a critical labour shortage across the country. “Make no mistake. This is a massive increase in economic migration to Canada,” Minister of Immigration, Sean Fraser told The Canadian Press. “We have not seen such a focus on economic migration as we’ve seen in this immigration levels plan.” According to Stats Canada, there is on average 1.1 unemployed people for each job vacancy in Canada in the second quarter, down from 1.3 in the first quarter, and from 2.3 in the second quarter of 2021. The lower the ratio, the tighter the labour market, as it indicates a smaller pool of applicants for each role, thus indicating further labour shortages. BC and Quebec lead the way with the tightest labour market at .8 unemployed people for each job vacancy.

Canada’s population is highly educated, with the largest share of college or university educated populations amongst the G7 countries. The population share with a bachelor’s degree or higher continues to rise with an influx of highly educated immigrants and a growing number of young adults completing degrees. In Q2, Canada’s population grew by the fastest rate in 55 years at .7%, an increase of 284,982 migrants, asylum claimants and permit holders, as well as people affected by the Russian and Ukraine conflict. While population growth via immigration is necessary to supplement Canada’s shortage of skilled labourers and aging work force, an increase at this rate could prove problematic for a country already suffering from a shortage of housing supply, thus causing increased competition in the rental market and higher rent costs.

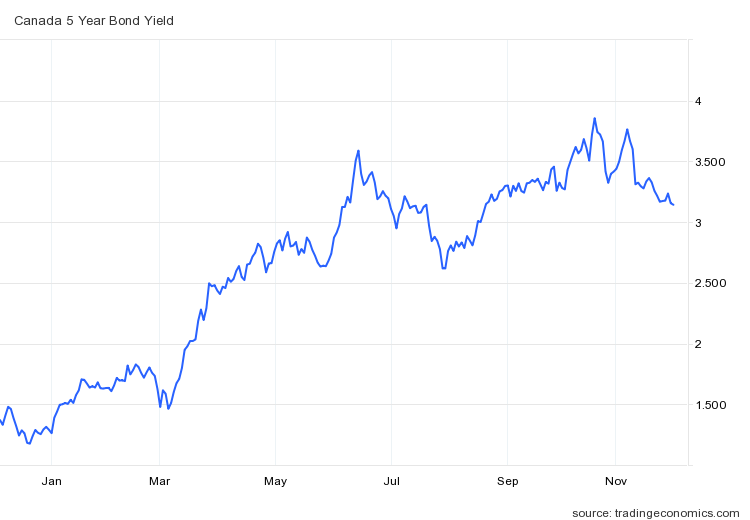

Bonds take a dip

5 year bond yields in November trended downwards closer to 3%, pushing Lenders to decrease long term fixed rates below 5% for the first time in nearly 6 months. We see no further incoming increases to fixed rates in the near term, variable rates will stagnate in 2023 and trend lower in 2024 once a Bank of Canada pivot takes place.

Inflation is still above the Bank of Canada’s target

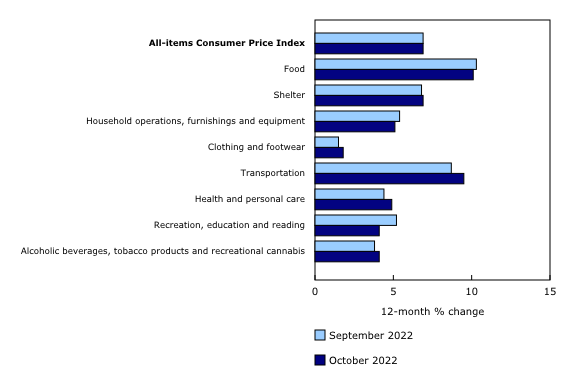

Consumer price index (CPI) for the month of September came in at 6.9%, excluding food and energy, prices rose 5.3% year over year in October in comparison to a gain of 5.4% in September. Year over year, prices rose at a faster pace in October compared with September in eight provinces. According to the Mortgage Interest Cost Index, as many are renewing at higher interest rates, mortgage interest costs increased on a year-over-year basis by 11.4%, the highest increase since February 1991 (+11.7%).

For potential homebuyers

If you’re looking to enter the market while housing prices have cooled our current best 5-year fixed rate is 4.70% and a 5-year variable rate of 5.30%.

For first-time home buyers, there are some great opportunities in a market dampened by negative sentiment and overall lack of competition.

For homeowners who are coming up for renewal, continue to monitor our rate forecasts, it would be wise to renew into shorter terms until rates begin to decrease in the coming year.

For homeowners who would like to see the benefit of switching lenders and breaking their mortgage early, Perch automatically calculates the net benefit once you input your existing property and mortgage details in your Perch portfolio.