Perch

Perch Est. reading time:

Est. reading time:

|

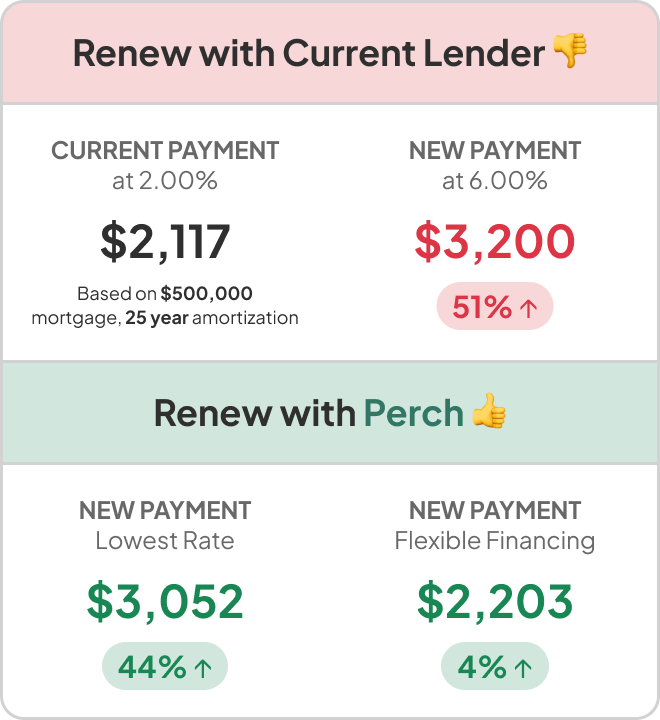

Save money on your mortgage. Learn about what your payment could be at renewal and how you can save by renewing your mortgage with Perch. |

Key Takeaways

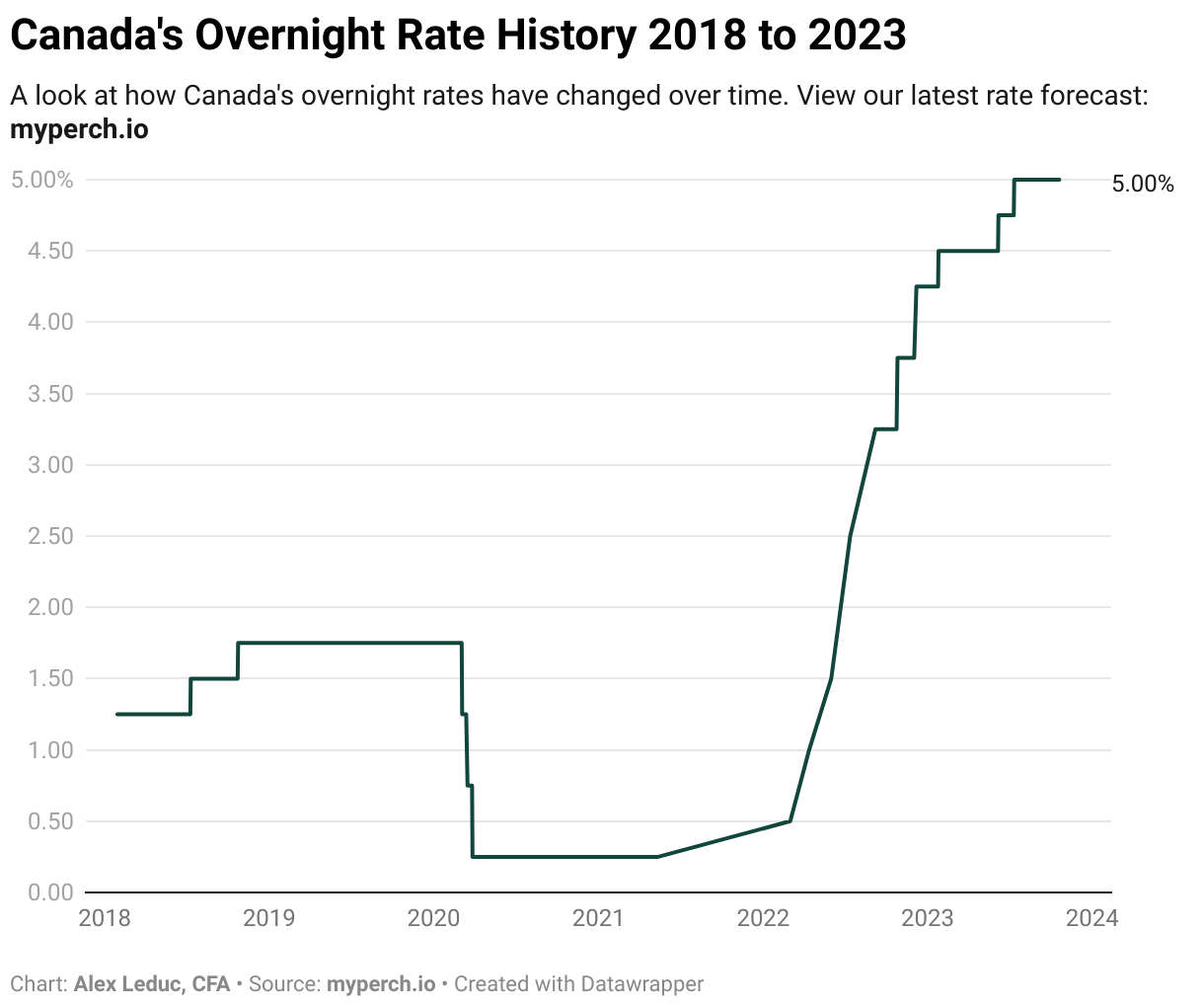

- The Bank of Canada has kept their policy interest rate steady at 5.00% as of their latest interest rate announcement

- The next interest rate announcement is on Wednesday, April 10, 2024.

- Our March mortgage outlook: fixed rates will continue drop and variable rates will remain the same.

- Talk to an experienced mortgage advisor to understand the announcement’s impact on your mortgage payment or upcoming renewal

Why did the Bank of Canada hold interest rates?

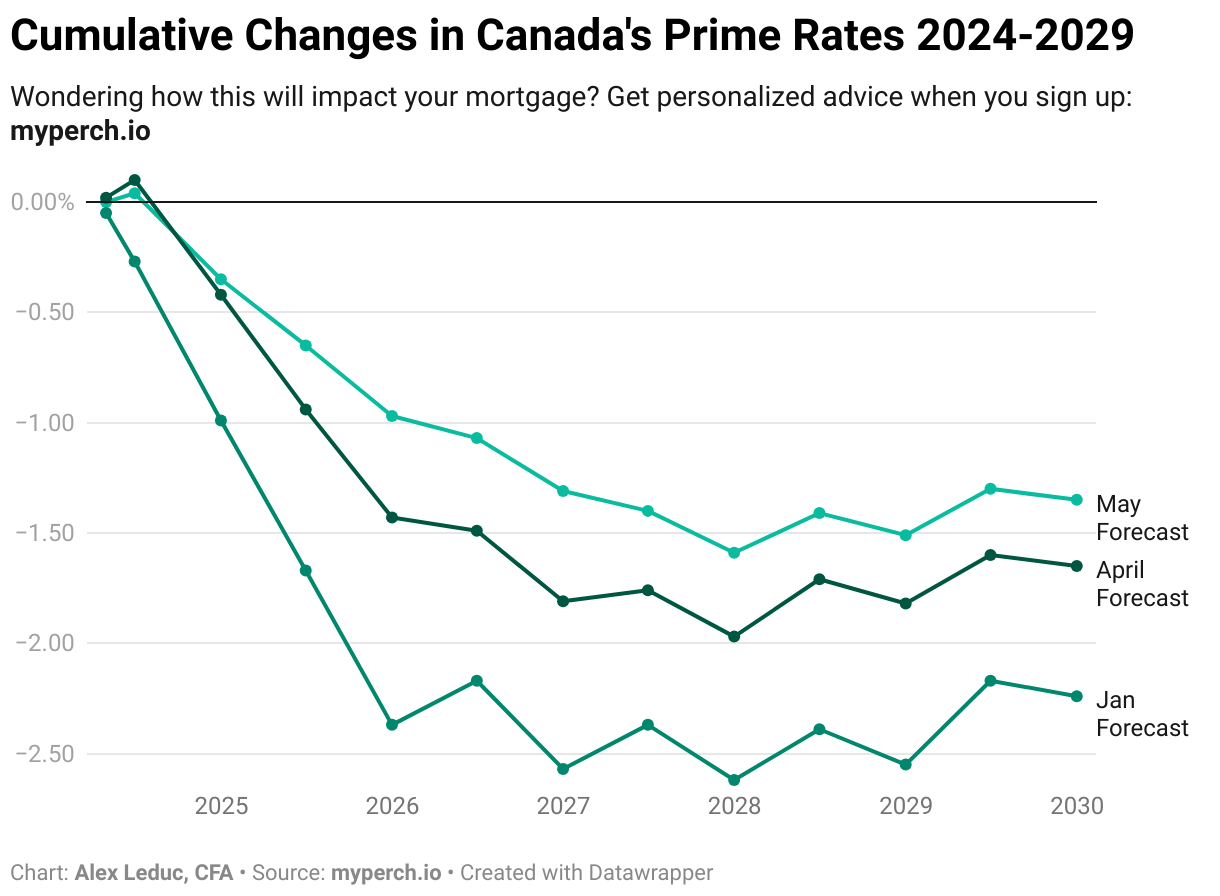

Commentary from Perch’s CEO and Principal Mortgage Broker, Alex Leduc: The latest Bank of Canada interest rate announcement occurred on March 6th. Inflation continues to trend in the right direction and the Bank of Canada doesn’t feel the need to intervene with any rate changes to throw off that momentum. The market is still expecting the first rate cuts in the second quarter of 2024. March is essentially the mid-point between the last two quarters, which reflects expected cuts to begin in the second half of 2024 at a pace of roughly 0.25% per quarter into 2026. Cumulative rate cuts of 2% are still expected between mid-2024 and the end of 2026. Inflation has been stickier than expected in the last few months, which has tempered expectations of earlier rate cuts. In the chart below, you can see how our 5-year variable rate forecast has changed over time based on the Bank of Canada interest rate announcements. (Like what you see? Sign up to get free, personalized mortgage insights and our monthly mortgage outlook!) The current focus for the Bank of Canada remains bringing inflation back in line with the targeted 2%. The Bank of Canada is anticipated to begin cutting rates in late 2024 to the end of 2026. During the next few years adjustable rate mortgage holders are likely to see lower payments. Related: Why are variable rates higher than fixed rates? Buying now gives you the opportunity to lock in a lower purchase price in today’s market, benefitting you in the long run. Think of it this way: You date the mortgage payment, but you marry the purchase price. In other words, your mortgage payment can fluctuate as you change terms, but your purchase price remains the same. We increasingly see new buyers opting for a shorter mortgage term with a higher amortization to minimize their monthly payments. This enables them to potentially renew at a lower rate a few years from now, and in the long run, accelerate their amortization to pay off their mortgage earlier.How will the latest Bank of Canada interest rate announcement affect home prices?

For March, we anticipate fixed rates will continue to drop and variable rates will remain the same. National sales activity continued to climb in January, +3.7 month over month, building on the +8.7% jump we saw in December, however, sales in January were still 9% below the 10-year average. On a year over year basis, sales activity is up 22% from January 2023, which was the worst start to a year in the past two decades. Canada’s inventory edged up by 1.5%, nowhere near inventory levels we’ve seen in the middle of 2023, thus, the sales-to-new listings ratio increased to 58.8% in January, up from 57.8% in December, in comparison, this ratio peaked at 67.9% in April. According to CREA, a ratio between 45% and 65% is generally consistent with a balanced housing market. “Sales are up, market conditions have tightened quite a bit, and there has been anecdotal evidence of renewed competition among buyers; however, in areas where sales have shot up most over the last two months, prices are still trending lower. Taken together, these trends suggest a market that is starting to turn a corner but is still working through the weakness of the last two years,” said Shaun Cathcart, CREA’s Senior Economist.The Aggregate Composite MLS Home Price Index edged down by a further 1.2% on a month-over-month basis in January, however it is up 0.4% year-over-year. The actual (not seasonally adjusted) national average home price was $659,395 in January, up 7.6% year over year.

Where will mortgage rates be in 2024?

According to financial models by Alex Leduc, Principal Broker at Perch, 5-year variable mortgage rates should start dropping in late 2024.

Will mortgage rates go up in the next 5 years?

Based on our latest Mortgage Rate Outlook, expect 5-year variable mortgage rates to start dropping in 2024 and continue doing so into 2025. We’ll be updating our mortgage rate forecast after every Bank of Canada interest rate announcement – you can subscribe to our mortgage rate forecast for free.

What is the Bank of Canada interest rate today?

The current Bank of Canada interest rate sits at 5.00%, with a 0.25% rate hike announced on July 12, 2023.When is the next Bank of Canada interest rate announcement?

The next scheduled Bank of Canada interest rate announcement is Wednesday, April 10th, 2024 at 10:00 AM ET.What are the interest rate announcement dates in 2024?

There are a total of 8 Bank of Canada interest rate announcements each year. The dates for 2024 are as follows:- Wednesday, January 24, 2024

- Wednesday, March 6, 2024

- Wednesday, April 10, 2024

- Wednesday, June 5, 2024

- Wednesday, July 24, 2024

- Wednesday, September 4, 2024

- Wednesday, October 23, 2024

- Wednesday, December 11, 2024