Ali

Ali Est. reading time:

Est. reading time:

Read the April 2023 Canada interest rate forecast.

Read the June 2023 Canada interest rate forecast.

The Bank of Canada has paused rate hikes for the time being, as inflation has began to slow in Canada. The Bank of Canada will be looking closely at economic data to determine whether or not they need to increase rates again to curb inflation or whether the current rate is enough to bring the CPI down. Let’s take a look at how the mortgage market is trending going into May.

Key Takeaways

- Bank of Canada has paused rate hikes for the time being, with the next announcement coming on June 7.

- We don’t anticipate major changes in fixed rates in May, with variable rates remaining steady.

- Today’s best mortgage rates are 4.34% for 5-year fixed and 5.66% on 5-year variable

- For buyers, there are great opportunities in the market, but sentiment seems to be turning around.

- For homeowners coming up for renewal, continue to monitor our rate forecast and avoid taking the first offer from your existing lender, as they’re typically less competitive.

How will mortgage rates trend in May?

Following the last rate hike in January 2023, the Bank of Canada has held rates steady for the past two policy announcements. For the month of May, we don’t anticipate major swings in fixed rates and variable rates will remain the same.

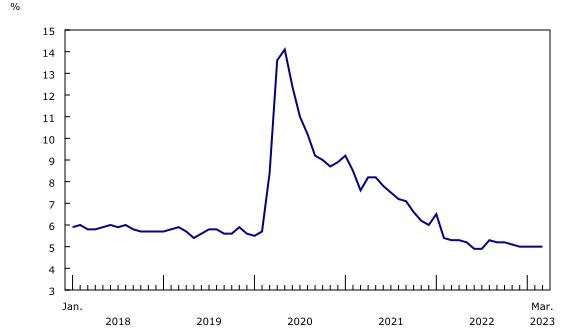

On April 12th, the BoC chose to hold their policy interest rate at 4.5% yet again, Lender prime rate remains unchanged at 6.7%. This decision came as no surprise, given the main focus of our Central Bank is to combat inflation which on a year over year basis has decreased quite significantly and faster than anticipated, albeit, mostly due to the base year affect, markets and economists are now shifting their focus to the 6-month CPI trend, which shows inflation is on the rise yet again, the culprit, higher mortgage interest rates. The next interest rate announcement is slated for June 7, markets have priced in another pause.

If you’re wondering why variable rates are now trending higher than fixed rates check out this article for a more in depth overview.

The housing market seems to have bottomed out

Home prices in major cities across Canada declined last year, following the Bank of Canada’s aggressive rate hikes. With rates paused for the time being and many analysts predicting a policy reversal later down the line, sentiment seems to be changing for the housing market. Canada’s national sales activity continues to rise (1.4% month over month) while the number of new supply levels remains at a 20-year low. Consecutive months of declining number of newly listed homes (-5.8% in March) has caused the sales-to-new listings ratio to reach a staggering 63.5%, marking the tightest market in a year, we expect April to trend similarly. The Aggregate Composite MLS Home Price Index (HPI) was up 0.2% on a month-over-month basis in March 2023, the first increase since February 2022, signaling price stability is ahead.

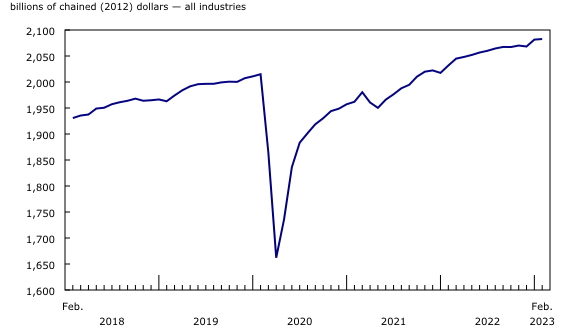

Economic growth has slowed but not declined

According to Statistics Canada real GDP rose by 0.1% in February, due to an increase in both services and goods-producing industries, on an annualized rate, real GDP grew by 2.5%. The bank of Canada, in its April monetary policy report estimates GDP will grow by only 1.4% annually for 2023 and highlights that we will not truly see the slowdown of the economy until later this year where “restrictive monetary policy continues to weigh on household spending, and business investment has weakened alongside slowing domestic and foreign demand.” The official first quarter Real GDP data will be available on May 31st.

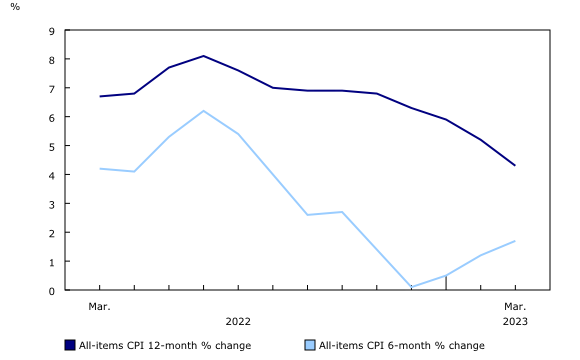

Inflation is slowing faster than expected

During the month of March, the CPI saw the biggest year over year deceleration since August 2021 (+4.1%). Following February’s 5.2% increase, March CPI rose 4.3% year over year. Excluding food and energy, prices increased 4.5% year over year and 3.6% when excluding mortgage interest cost. Gasoline prices have contributed strong downward impact on consumer inflation all while rising mortgage interest rates continue to apply serious upward pressure on the CPI. Canadians shopping for a new home or renewing their mortgage today are experiencing a 26.4% increase in mortgage costs versus a year ago, the largest yearly increase on record. We expect the CPI to continue its declaration in April below 4% and trend closer to the Bank of Canada’s revised inflation outlook of 3% by June.

How is the job market doing?

According to Stats Canada Job vacancies decreased by 4% in February, the lowest since August 2021, this puts the job vacancy rate at 4.7%. The decline in job vacancies was led by the health care and social assistance as well as educational services sectors.

Canada added 35,000 new jobs in March, lead by growth in the private sector, an increase from the 22,000 jobs added in February, once again, passing expectations. The unemployment rate continues to hold at 5%, for the fourth consecutive month, which should begin to increase in the coming months as higher interest rates continue to work their way into the economy.

Average weekly earnings grew 5.4% year-over-year in February, up from January (4.5%). The central Bank anticipates weaker economic growth in the upcoming quarters to ease pressures in the labour market and moderate wage growth however warning that “unless a surprisingly strong pickup in productivity growth occurs, sustained 4% to 5% wage growth is not consistent with achieving the 2% inflation target.”

Canada’s population growth may be playing a part in inflation

The Central Bank continues to warn that strong population growth is supporting aggregate consumption and employment growth all while the Federal Government continue to push for their goal of 1.4 million new immigrants in the next 3 years. Canada’s population grew by just over 1 million people in one year for the first time since 1957, this puts Canada’s estimated population at nearly 40 million with a 2.7% annual population growth.

The bond market is predicting a recession

After a sudden stampede into safer assets in the month of March on the news of failing international banks and a potential liquidity crisis, April bond yields activity was lackluster, holding around 3% for the most part. The bond market is pricing in a higher risk of a recession on the back of a potential credit crunch.

Is now the right time to buy a home?

With rate hikes paused and the housing market down across the board in cities, now might be the time to jump on the homeownership bandwagon if you’ve been waiting on the sidelines.

When interest rates eventually come down again it’s likely the increased demand will bring the housing market back to where it was pre 2022. If you go with a variable rate you could have the best of both worlds when rates come back down, or you could play it safe and go with a fixed rate mortgage.

Our current best 5-year fixed rate is 4.34% and 5-year variable rate of 5.66%.

For first-time home buyers, there are some great opportunities outside of core cities, however as the narrative begins to change and the negative sentiment subsides, expect higher competition, especially as inventory is at 20-year lows.

For homeowners who are coming up for renewal, continue to monitor our rate forecasts, it would be wise to see what rates Perch may be able to offer above and beyond your existing Lender, as they’re typically less aggressive on their rate offerings.

For homeowners who would like to see the benefit of switching lenders and breaking their mortgage early, Perch automatically calculates the net benefit once you input your existing property and mortgage details in your Perch portfolio.