Ali

Ali Est. reading time:

Est. reading time:

Read the 2024 interest rate forecast.

Save money on your mortgage

Don’t leave money on the table

Don’t just go with your bank

Get today’s best rates from our lenders

On October 25th, The Bank of Canada published their Monetary Policy Report accompanied by decision to hold their Policy interest rate at 5.00%. With only one final meeting set for December 6th, it is now widely expected that the Central Bank will close off 2023 with another rate hold, keeping at the current 5.00% Policy interest rate. Let’s take a look at the latest in the mortgage world going into December.

Commentary from Perch's CEO and Principal Mortgage Broker, Alex Leduc:

As a result of recent data showing inflation continuing its deceleration towards the Bank of Canada's target and slow economic growth, the market now predicts no further rate hikes. Instead, it anticipates that rate cuts will likely start in the second half of 2024. While the pace of rate cuts is largely unchanged at approximately 0.25% per quarter over 1.5 years, the long-term normal interest rate has decreased by 0.50% compared to October's outlook.

Various sources estimate that 60% of mortgages are set to renew by 2026. Good news for borrowers: Anticipated rate reductions of about 1% in 2025 and 1.5% in 2026 will help ease the impact of higher rates during renewal.

Key Takeaways

- The Bank of Canada has paused rate hikes for the time being, with the last interest rate announcement scheduled to be on December 6th, 2023.

- Today’s best mortgage rates are 5.34% for 5-year fixed and 6.01% for 5-year variable.

- For first-time home buyers, there are some great opportunities, sellers are coming to terms with tapering price growth as higher interest rates bar many from entering the market, inventory has increased, but will taper off going into the remainder of 2023, before ramping up in 2024.

- For homeowners who would like to see the benefit of switching lenders and breaking their mortgage early, Perch automatically calculates the net benefit once you input your existing property and mortgage details in your Perch portfolio.

- For homeowners coming up for renewal, continue to monitor our rate forecast and avoid taking the first offer from your existing lender, as they're typically less competitive.

What's new in the mortgage world for December?

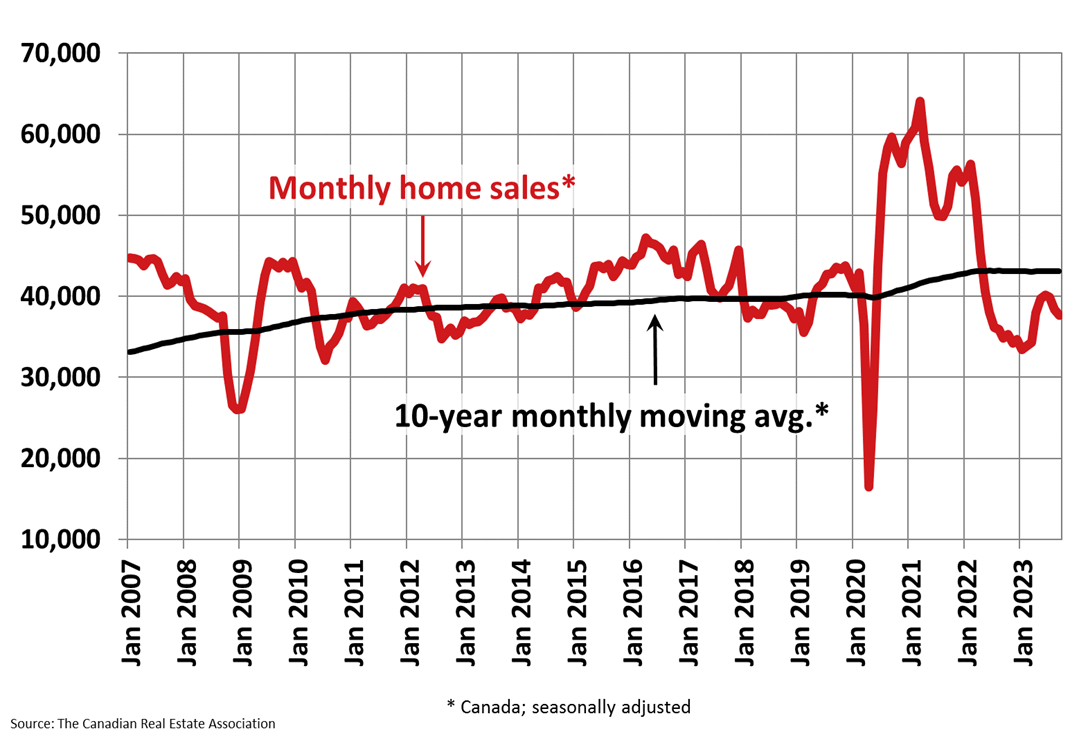

For the month of December, we anticipate fixed rates will drop and variable rates will remain the same. National sales activity edged down further in October by 5.6% month over month, remaining on trend with August’s and September’s declining sales activity. Canada’s inventory edged down by 2.3% month over month in October, the first decline we’ve seen since March. Sales activity has officially tapered off and inventory is now on a seasonal decline, thus the sales-to-new listings ratio eased to 49.5% in October, a 10 year low, in comparison, this ratio peaked at 67.9% in April.

“We know housing demand is extremely high all across the country, but October’s resale data was further confirmation that it probably won’t be manifesting itself in the existing home market for the remainder of this year and likely not until spring 2024 at the earliest,” said Shaun Cathcart, CREA’s Senior Economist.

The Bank of Canada is continuing to hold interest rates steady

On October 25th, The Bank of Canada published their Monetary Policy Report accompanied by decision to hold their Policy interest rate at 5.00%. With only one final meeting set for December 6th, it is now widely expected that the Central Bank will close off 2023 with another rate hold, keeping at the current 5.00% Policy interest rate. There has been an increase of 75 basis points to the Bank of Canada’s overnight lending rate in 2023, a notable but small increase in comparison to 2022’s 400 basis point run. The Central Bank believes there’s now sufficient evidence pointing to slowing demand and increased probability of a recession, lead by slower consumption growth and a decline in housing activity, while still maintaining their hawkish and precautionary stance. Markets and Senior Economists are largely convinced there are no more rate hikes in the pipeline for Canadians and expect the first rate drop to come as soon as Q2. The Central Bank projects the economy will continue to cool down, bringing inflation back to its two per cent target some time in early 2025.

The strength of the Canadian economy

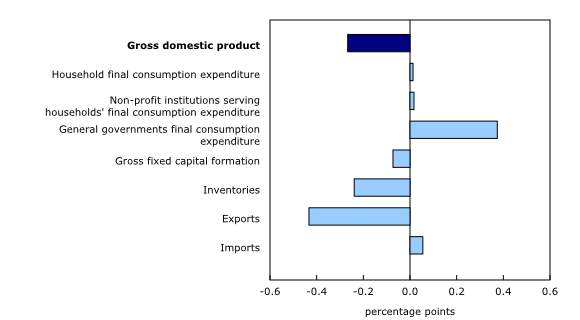

Q3 negative GDP data released on November 30th shows that on an annualized basis, the Canadian economy contracted at a rate of 1.1%. Statistic Canada has also revised their previous Q2 data from a 0.2% decline to a 1.4% gain on an annualize basis. While this technically means Canada is not yet in a recession, as we have not yet had two consecutive contracting quarters, growth stalled, remaining essentially unchanged and coming in well below expectations. "We expect the economy to remain weak for the next few quarters," Bank of Canada Governor Tiff Macklem said, "The excess demand in the economy that made it too easy to raise prices is now gone." he added. The Canadian economy continues to move against expectations of an incoming slowdown, Stats Canada say early estimates state that we will see growth of 0.2% in Q4.

Key Terms:

GDP: GDP or Gross Domestic Product refers to the total dollar amount of goods and services produced in a country. It is an overall measure of the strength of our economy.

CPI: The CPI or Consumer Price Index is a measure of inflation tracked by Statistics Canada. It attempts to track the spending habits of the average consumer with a basket of typical goods and services.

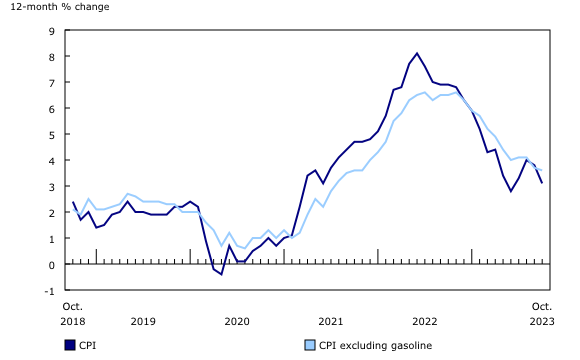

Inflation trends down, but remains above target

October’s consumer price index, the measure for year over year inflation, came in at +3.1%, following a 3.8% year over year increase in September. October’s drop was mainly driven by a month over month drop in gasoline prices (-7.8%), gas prices are expected to continue to drop in November and potentially further in December. Canadians continued to battle elevated shelter costs (+8.2%) and mortgage interest costs (+30.5%) in October and beyond, notably, mortgage interest rates has been and continues to apply the highest upward pressure on the CPI since December of 2022.

The Central Bank sees tightening household discretionary spending as their most viable tool to halt consumer spending on goods and services and attain their 2% inflation target, the CPI will drop below the 3% mark in November, the next slated CPI announcement will be on December 19.

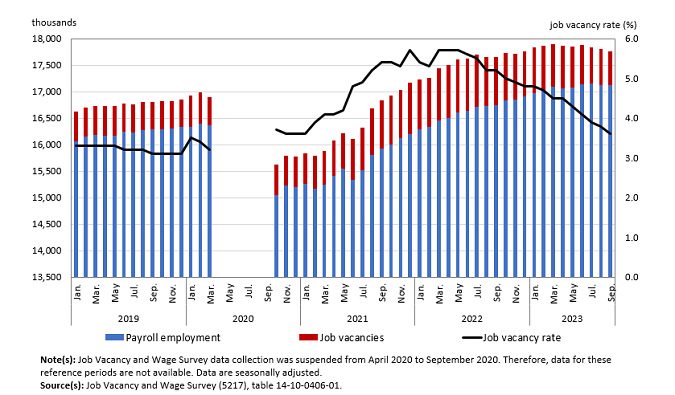

Job vacancies and Unemployment Rates

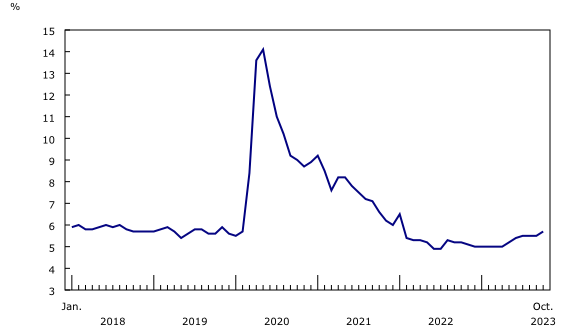

Following an increase of 64,000 job in September, Canada’s employment rose by a further 18,000 jobs in October, falling short of estimates of 25,000 jobs. The increase in jobs was led by construction (+23,000; +1.5%) and an increase in information, culture and recreation (+21,000; +2.5%),. The job gains were offset by decreases wholesale and retail trade (-0.7%) and manufacturing (-1.0%). Canada’s continued increase in newcomers has been the biggest prop up to our job market, however the unemployment rate still managed to edge up in October at 5.7% after remaining at 5.5% for three consecutive months.

Job vacancies continued to decline, by 40,700 in the month of September, there were 1.9 unemployed persons for every job vacancy in Canada, up from 1.8% in August, indicating the labour market tightness has eased, which will reduce upward pressure on wage growth.

Strong population growth continues to fuel demand

Strong population growth continues adding both demand and supply to the Canadian economy, newcomers are helping ease the shortage of workers while also boosting consumer spending and driving up demand for housing. Ottawa plans to level out the number of new immigrants it accepts in 2026, however will maintain their goal of attracting 500,000 newcomers annually in both 2024 and 2025. Many arriving in Canada’s major markets are searching for shelter amidst the home unaffordability crisis, driving up rental cost (+8.2%) in October. Provinces rely heavily on Canadian investors to supply rental apartments in the form of investment homes, however, as higher interest rates and mortgage costs have worked to deter existing and would be landlords, the supply of rentals has steadily declined which has driven up rents across the country.

Recommended reading: How does population affect the housing market?

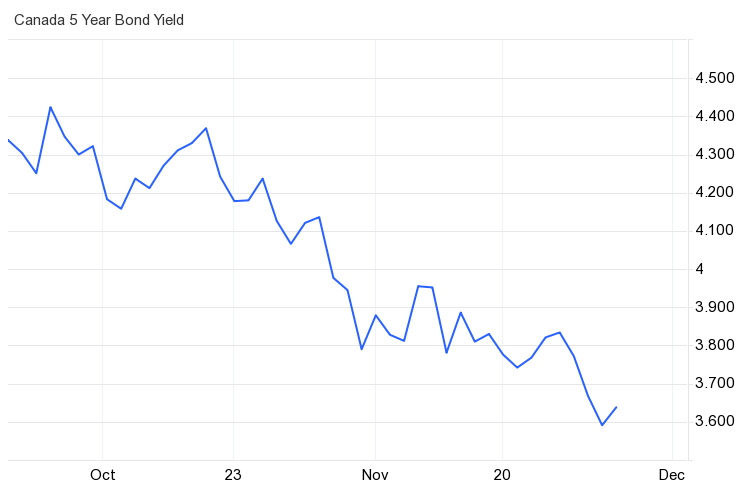

Bond yields retrace their gains

Canada’s 5-year bond yields have plummeted over 80 basis points since they reached 16-year highs during the month of October. Canada's mortgage rates tend to track five-year bond yields at a premium and with a lag. Yields dropped due to a growing consensus of interest rates remaining elevated long than anticipated and a hard Canadian recession fears all but diminished as the Canadian economy is now expected to be in a mild recession after a flat Q2 and a negative Q3.

If you’re looking to buy a home in Canada:

For first-time home buyers, there are some great opportunities, sellers are coming to terms with tapering price growth as higher interest rates bar many from entering the market, inventory has increased, but will taper off going into the remainder of 2023, before ramping up in 2024.

For homeowners who are coming up for a mortgage renewal, continue to monitor our rate forecasts, it would be wise to see what rates Perch may be able to offer above and beyond your existing Lender, as they’re typically less aggressive on their rate offerings.

For homeowners who would like to see the benefit of switching lenders and breaking their mortgage early, Perch automatically calculates the net benefit once you input your existing property and mortgage details in your Perch portfolio.