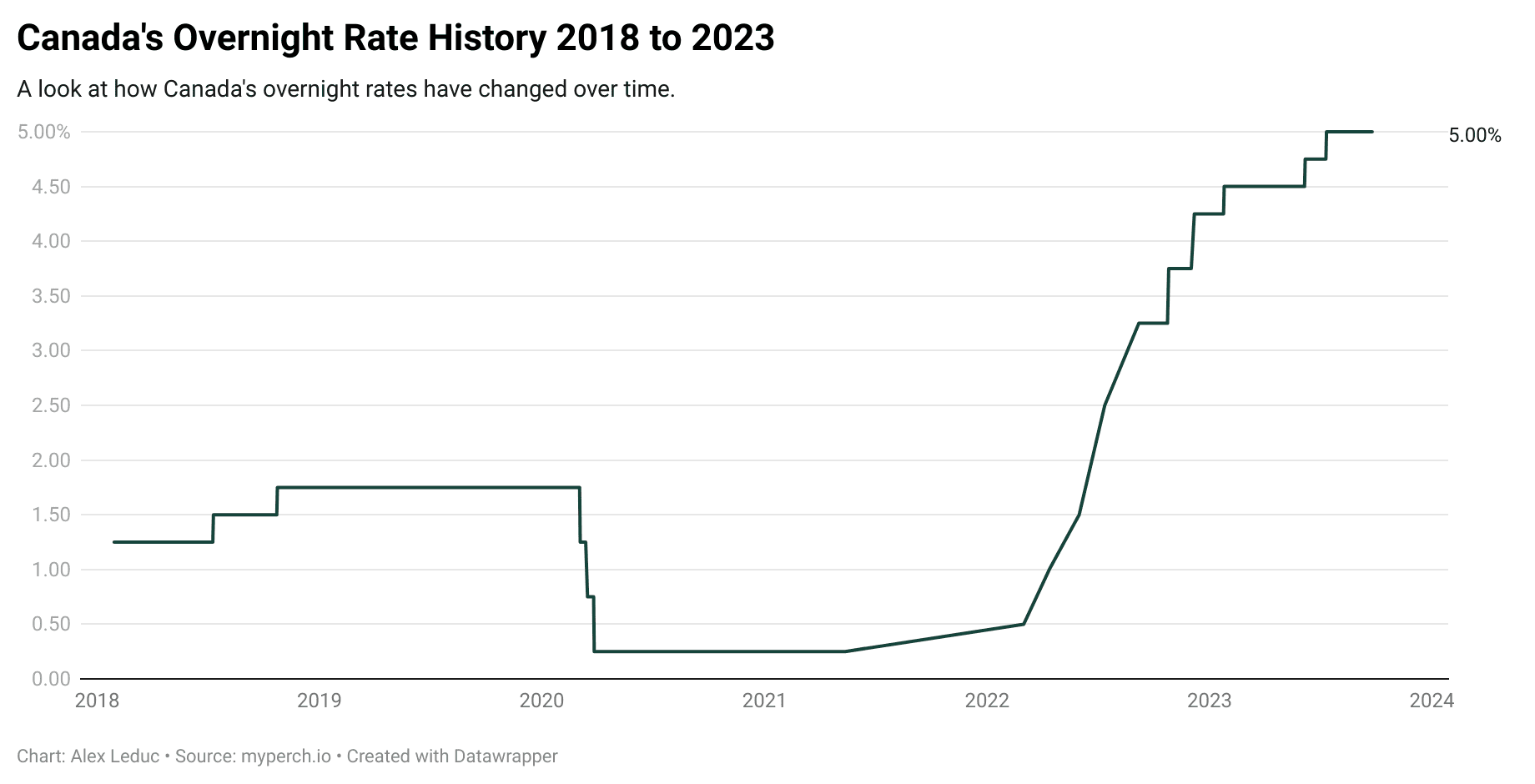

Canada Interest Rate Forecast 2025-2028

Last Updated: April 16, 2025

CURRENT INTEREST RATE FORECAST FOR 2024: 2.75% (last updated April 16, 2025)

Current Forecasts:

For more information about the 2024 Bank of Canada rate announcement schedule, read more here 👈

Key Takeaways (updated April 2025)

- On Wednesday, April 16, 2025, The Bank of Canada announced that it will be holding its rate, keeping the policy rate at 2.75%.

- Recent data indicates inflation is decelerating toward the Bank of Canada’s target, coupled with slow economic growth.

2025 Predictions (updated April 2025)

- An additional 0.75%-1% of cuts is expected for the remainder of 2025, but we then expect a few hikes in 2026 and onwards since we are currently at the expected long-term rate.

Will Interest Rates in Canada Go Down in 2025?

On April 16th, the Bank of Canada cut its interest rate to 2.75%. The next Bank of Canada announcement is scheduled for June 4, 2025.

Commentary from Perch’s CEO and Principal Mortgage Broker, Alex Leduc:

- The Canadian economy is showing moderate growth, core inflation spiked to 2.7% (from 2.1% the prior month) is well above the 2% target and tariffs are expected to apply upward pressure on inflation for the near future. As a result, the Bank of Canada has paused rate cuts to avoid fueling inflation’s rise any further.

When is the next Bank of Canada rate increase and what can I expect?

The current market overnight interest rate forecast for the remainder of 2025 is:| Variable Rate Interest Forecast 2025 to 2028 (as of April 2025) | |

|---|---|

| Date | 5-year variable rates |

| 3/31/25 |

4.00% |

| 6/30/25 |

3.83% |

| 12/31/25 |

3.13% |

| 6/30/26 |

3.97% |

| 12/31/26 |

3.48% |

| 6/30/27 |

3.60% |

| 12/31/27 |

3.60% |

| 6/30/28 |

3.71% |

| 12/31/28 |

3.74% |

| 6/30/29 |

3.82% |

| 12/31/29 |

3.86% |

How will the latest Bank of Canada interest rate announcement impact your monthly mortgage payments?

- For variable rate mortgages (meaning your payments don’t fluctuate as prime rates change): Your existing mortgage payments will remain unchanged. Use our Mortgage Renewal Calculator to get an estimation of what your expected rate and payment will be at your maturity date. If the payment isn’t manageable, connect with your advisor well in advance to look at all options.

- For adjustable rate mortgages (meaning your payments fluctuate as prime rates change): Your payments will remain unchanged for now, but the outlook shows that a few more cuts from the Bank of Canada are expected throughout 2025 to further reduce your mortgage payments.

What is the interest rate forecast for 2025 in Canada? (updated April 2025)

Commentary from Alex Leduc, Principal Mortgage Broker and CEO of Perch:

- The Canadian economy is showing moderate growth, core inflation spiked to 2.7% (from 2.1% the prior month) is well above the 2% target and tariffs are expected to apply upward pressure on inflation for the near future. As a result, the Bank of Canada has paused rate cuts to avoid fueling inflation’s rise any further.

What is CPI and how does it affect the Canada interest rate forecast?

CPI stands for consumer price index and it is the measure of average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. It is mainly used to measure inflation. A rising Consumer Price Index (CPI) would prompt the central bank to raise interest rates. The CPI basket includes 8 main categories of goods and services: Food, Shelter, Household operations, Clothing, Transportation, Health, Recreation, and Alcoholic beverages. CPI data is reported for various geographic areas, including Canada, provinces, and select cities, such as Whitehorse, Yellowknife, and Iqaluit.

What affects the Bank of Canada’s interest rate forecast?

We look at some of the core factors that the Bank is monitoring to gauge which direction they are likely to go. In this case, all indicators seem to indicate they will hold.- Real GDP Growth: The Bank of Canada is expecting GDP growth of 1.8% in 2025 and 2026. This is an acceptable amount of GDP growth and would support a hold. (Source: Bank of Canada)

- Inflation: Core inflation (year over year) in January was 2.1% (vs 1.8% in December), slightly above the Bank’s 2% inflation target and is trending upward, which would support a hold. (Source: Trading Economics)

- Unemployment: Decreased to 6.6% in January (0.9% higher than 1 year ago). This downward trend in the past few months would justify a hold. (Source: Trading Economics)

What is the Canadian prime rate?

The prime rate is what major banks and financial institutions in Canada use to set interest rates for loans and lines of credit which also include variable rate mortgages.

Is prime rate the same as mortgage rate?

The prime rate is not the same as your mortgage rate. A prime rate is the base cost of borrowing from which lenders start to determine interest rates on mortgages, personal loans, credit loans or other financial products. In general, the prime rate mostly affects variable rate mortgages. Your mortgage rate is the interest rate you are expected to pay on any borrowed money.

What is the mortgage interest rate forecast for 2025 in Canada?

On April 16th, the Bank of Canada announced a rate hold, keeping the interest rate at 2.75%.

Our current best 5-year fixed rate is 3.84% and 5-year variable rate is 4.10%.

What are the interest rate predictions from the banks?

CIBC

Economist Avery Shenfield predicts two more 25-basis-point rate cuts, bringing the overnight rate to 2.25%. He suggests this could be the cycle’s low—if Canada and the U.S. reach a tariff-removal deal by summer, which remains his base case. However, a prolonged trade war could trigger a major recession, with further rate cuts depending on fiscal policy support and whether rising prices are tempered by inflationary pressure from economic slack.

RBC

RBC Economists predict the Bank of Canada will continue cutting rates, with a base case of 2.25% by mid-year. The latest 25bps cut to 2.75% was widely anticipated due to U.S. trade risks, though stronger economic data had suggested a hold was possible. While the BoC acknowledges economic resilience, trade uncertainty is dampening business investment and hiring. Inflation has ticked up, but the central bank remains focused on its long-term target. Governor Macklem emphasized that monetary policy cannot fully offset trade disruptions, and future rate decisions will depend on economic data, inflation trends, and potential fiscal responses.

Scotiabank

Scotiabank economists predicted that the Bank of Canada would cut rates by 25bps on March 12. No new forecasts or Monetary Policy Report were issued, with the next update expected in April. While quantitative tightening ended in January, balance sheet growth through repos and bills continued. The BoC may have held rates if not for tariffs, but their impact alone did not ensure further easing.

TD Canada

TD economists view the key implications as follows: The Bank of Canada is taking precautionary measures against prolonged tariffs, which are expected to weigh heavily on the economy. While strong recent data could have justified a pause, the trade war narrative now dominates. TD’s updated forecast anticipates a shallow recession, assuming Canadian exporters face a 12.5% effective tariff for at least six months—a sharp increase from below 2% previously. With tariff pressures persisting, the BoC is likely to maintain a dovish bias, with the overnight rate projected to reach 2.25% by June, though further cuts may be constrained by inflation risks.

BMO

BMO Economist Douglas Porter states that the Bank of Canada continues to strike a balanced tone in its response to the trade war, acknowledging both the downside risks to growth and the upside risks to inflation. However, he strongly suspects that the growth slowdown will prevail, and while the Bank’s cautious approach means it will move slowly, the ultimate destination for rates will likely be lower than the market currently expects—especially if the trade war escalates beyond the planned U.S. tariffs.

Alex Leduc

Alex Leduc is Founder and CEO at Perch. Prior to starting Perch, he worked in the real estate sector for 8 years in corporate finance, strategy and analytics roles. He is currently a Technical Advisory Committee Member of the Financial Services Regulatory Authority of Ontario (FSRA) and Co-Chair of the Canadian Lenders Association Mortgage Roundtable. Alex is a graduate of Ivey Business School from Western University and a CFA Charterholder. LinkedIn