Alex

Alex Est. reading time:

Est. reading time: Home buyers looking for desperate sellers who can’t cover their increased mortgage payments at renewal may be waiting for nothing. Despite recent news headlines, homeowners who purchased in the past 5 years can afford to ride it out.

Mortgage rates have come up quickly in 2022, there’s no doubt about that. This has fueled speculation that interest rates will keep rising and Canadian homeowners won’t be able to handle increased mortgage payments. To analyze this properly, we’re going to look at the average first-time home buyer profile (who would arguably be the most exposed) over the past 5 years, from 2017 to 2022, and then simulate what the expected impact is when they come up for mortgage renewal.

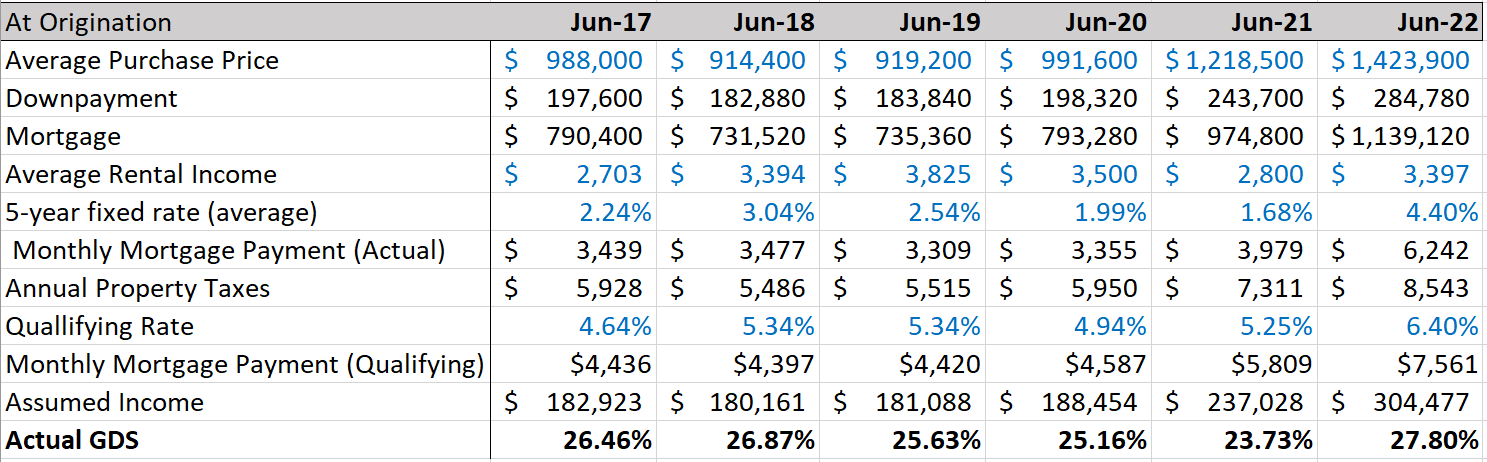

We’ve assumed a semi or detached property in the Greater Toronto Area[1], had a 20% down payment[2], went with the average 5-year fixed rate[3] at that time with a 25-year amortization[4] and bought below their max qualifying amount[5]. Here is a typical buyer profile for the past 5 years:

The average purchase price for our buyers is shown by year between 2017-2022. Based on the qualifying rates at that time for the mortgage stress test, we then calculated what qualifying income would be required for that household to get the mortgage they needed at 20% down payment. While the qualifying mortgage payment will impact affordability, the actual mortgage payment is the true cost to the borrower since that is what they pay, and we capture this with Actual GDS (gross debt servicing ratio).

Key Takeaways

- Historically the mortgage, property taxes and utilities for this buyer ranges between 23.7%-27.8% (actual GDS) of their gross household income.

- From 2017-2020, the required household income to qualify remained roughly the same since home prices didn’t fluctuate much. However, in the past 2 years you can see accelerating home prices and steep increases in qualifying rates have dramatically increased the qualifying income required to buy the same home. This should lead to less resale properties (since most people wouldn’t qualify for the property they already have, let alone be able to upgrade to another property in the same city). This has already started to materialize through record de-listings.

- We should also see extremely high rates of mortgage renewals with their existing lender (where you don’t have to re-qualify under the stress test), since people will find it more difficult to qualify to switch mortgage lenders.

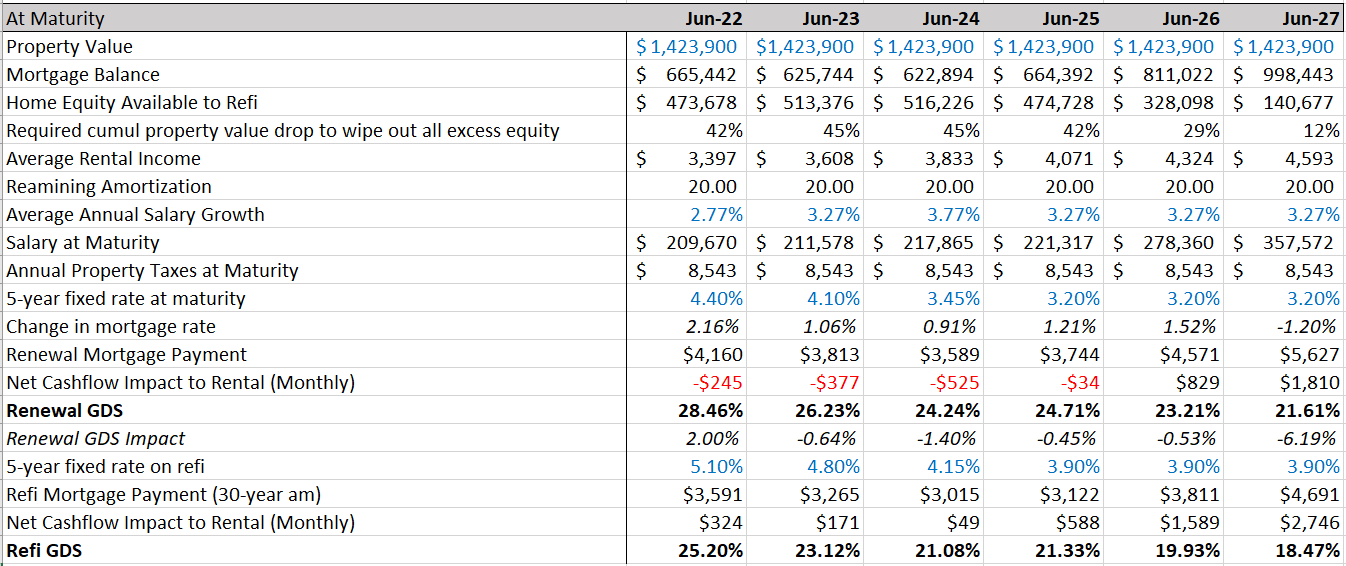

To look at the impact on mortgage renewals, we factor in what their new mortgage payment (using market data to estimate future 5-year fixed rates) and property taxes would be, along with what their changes in income would look like to offset the higher mortgage expenses.

The property value won’t materially affect the renewal rate, so we remove any of the effects of property growth.

Key Takeaways

- People renewing their mortgage in 2022 should have the hardest adjustment, with a 2% increase in GDS. In other words, an additional 2% of their gross income must go towards their mortgage payments. However, a 2% difference isn’t substantial and as you can see every year after 2017 has a lower impact. People getting a mortgage in 2022 would actually experience a relative improvement in cashflow serviceability when they renew in 2027.

- With a remaining amortization of 20 years at maturity, anyone who can’t service the higher mortgage payments could leverage a home equity line of credit (HELOC) to convert their payment into interest-only or refinance (if they qualify) up to a 30-year amortization to minimize their mortgage payments. Through either of these methods, a homeowner would be able to maintain or reduce their monthly mortgage payment, compared to when they first purchased. In other words, this means mortgage affordability would improve. If someone doesn’t qualify with their current lender, they are almost certain to qualify with an alternative lender which has substantially higher qualifying thresholds.

- In a worst-case scenario, if someone didn’t qualify for any lender, they could leverage their home equity through a private mortgage to cover the monthly shortfall and then refinance at renewal to pay it out. To wipe out any excess home equity, the cumulative property declines for the next 4 years would have to be around 43%, which is highly unlikely.

- We also looked at if the property was a rental, the rapid increases in rental income and ability to refinance offer a similar result. The owner would be able to offset any impacts to cashflow (ignoring their higher income) by refinancing and any buyer after 2021 is expected to improve their cashflow on renewal.

In summary, most buyers in the past 5 years will have their mortgage mature and the relative impact as a percentage of income is not material. They also have several options at their disposal to help with cashflow as a result of built-up home equity or the ability to re-amortize their mortgage while they ride out this higher rate environment which is expected to pass.

Buyers who are on the sidelines assuming these owners will fire sale their properties will be disappointed because we’ll see less properties listed as homeowners choose to stay put. If the right property comes along, now is an opportune time to enter the market if you qualify. Even if you don’t qualify, you could leverage an alternative lender (typically 1-1.5% more expensive on the mortgage rate) for a 1 to 3 year term until you can refinance out to a prime lender.

[1] Using average home prices from CREA

[2] According to Mortgage Professionals Canada, the average down payment on a purchase is closer to 24% and roughly 50% of first-time homebuyers put down less than 20%. We assumed 20% to be conservative.

[3] Around 70-75% of buyers get a fixed rate on their mortgage and if anyone got a variable rate most of the qualifying rate assumptions we made to arrive at our conclusion would be unchanged.

[4] According to Mortgage Professionals Canada, the average amortization is closer to 22 years with only 14% of buyers going above a 25-year amortization. We assumed 25 years to be conservative.

[5] We define this as 33% of their pre-tax income is going towards their qualifying mortgage payment, property taxes and utilities, which is below the standard maximum of 39% mandated by the stress test and supported by our funded data.