Ali

Ali Est. reading time:

Est. reading time:

Read the 2024 interest rate forecast.

Save money on your mortgage

Don’t leave money on the table

Don’t just go with your bank

Get today’s best rates from our lenders

On June 5th, The Bank of Canada published their decision to cut their Policy interest rate by 25 basis points. Markets and the Central Bank are convinced now there’s sufficient evidence pointing to slowing demand and an economy in modest excess supply, led by slower consumption growth and a decline in housing activity. Markets and Senior Economists are largely convinced there are more rate cuts in the pipeline for Canadians and expect two additional 0.25% cuts to occur in the second half of this year and cumulative cuts of 2% by the end of 2025. The Central Bank projects the economy will continue to cool down, bringing inflation close to 2% during the first half of this year. The Bank of Canada will be publishing their Interest rate announcement and Monetary Policy Report on their third meeting of 2024, on July 24th, when many are speculating a further 25 basis point rate cut.

Commentary from Perch’s CEO and Principal Mortgage Broker, Alex Leduc:

With GDP growth coming in under expectations and inflation within striking distance of the Bank of Canada’s target , they’ve ruled that it’s time to ease off some of the financial pressure. This is the first (and hopefully not the last) cut of 2024, with 1 more expected cut by year end.

Key Takeaways

- The Bank of Canada has cut their policy interest rate, which brings it to 4.75% as of their latest interest rate announcement.

- For the month of June, we anticipate fixed rates will continue to decrease and variable rates will also trend lower as Lenders adjust their prime rate following the 25-basis point rate cut issued by the Bank of Canada.

- Today’s best mortgage rates are 4.70% for 5-year fixed and 5.85% for 5-year variable.

- For first-time home buyers, there are some great opportunities, sellers are coming to terms with tapering price growth as higher interest rates have barred many from entering the market, inventory is increasing and will edge up in the middle months of 2024.

- For homeowners who are coming up for renewal, continue to monitor our rate forecasts, it would be wise to see what rates Perch may be able to offer above and beyond your existing Lender, as they’re typically less aggressive on their rate offerings.

- For homeowners who would like to see the benefit of switching lenders and breaking their mortgage early, Perch automatically calculates the net benefit once you input your existing property and mortgage details in your Perch portfolio.

What’s new in the mortgage world this month?

For the month of June, we anticipate fixed rates will continue to decrease and variable rates will also trend lower as Lenders adjust their prime rate following the 25-basis point rate cut issued by the Bank of Canada. National sales activity dropped by 1.7% month over month in April, remaining below average compared to the last 10 years. Actual (not seasonally adjusted) monthly activity came in 10.1% above April 2023.

“April 2023 was characterized by a surge of buyers re-entering a market with new listings at 20-year lows, whereas this spring thus far has been the opposite, with a healthier number of properties to choose from but less enthusiasm on the demand side,” said Shaun Cathcart, CREA’s Senior Economist.

Canada’s inventory edged up by 2.8% in April, nowhere near inventory levels we’ve seen in the middle of 2023, thus, the sales-to-new listings ratio edged down to 53.4% in April, down from 58.8% in January, in comparison, this ratio peaked at 67.9% in April 2023. According to CREA, a ratio between 45% and 65% is generally consistent with a balanced housing market.

“Mortgage rates are still high, and it remains difficult for a lot of people to break into the market but, for those who can, it’s the first spring market in some time where they can shop around, take their time and exercise some bargaining power. Given how much demand is out there, it’s hard to say how long it will last.” said James Mabey, newly appointed Chair of CREA’s 2024-2025 Board of Directors.

The Aggregate Composite MLS Home Price Index was flat on a month-over-month basis in April, however it is down 0.9% year-over-year. The actual (not seasonally adjusted) national average home price was $703,446 in April, down 1.8% year over year.

The Bank of Canada is cuts interest rate

On June 5th, The Bank of Canada published their decision to cut their Policy interest rate by 25 basis points. Markets and the Central Bank are convinced now there’s sufficient evidence pointing to slowing demand and an economy in modest excess supply, lead by slower consumption growth and a decline in housing activity. Markets and Senior Economists are largely convinced there are more rate cuts in the pipeline for Canadians and expect two additional 0.25% cuts to occur in the second half of this year and cumulative cuts of 2% by the end of 2025. The Central Bank projects the economy will continue to cool down, bringing inflation close to 2% during the first half of this year. The Bank of Canada will be publishing their Interest rate announcement and Monetary Policy Report on their third meeting of 2024, on July 24th, when many are speculating a further 25 basis point rate cut.

Key Terms:

GDP: GDP or Gross Domestic Product refers to the total dollar amount of goods and services produced in a country. It is an overall measure of the strength of our economy.

CPI: The CPI or Consumer Price Index is a measure of inflation tracked by Statistics Canada. It attempts to track the spending habits of the average consumer with a basket of typical goods and services.

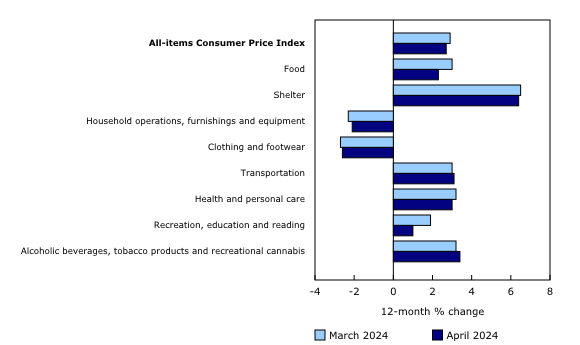

Consumer price index (CPI)

April’s consumer price index, the measure for year over year inflation, came in at +2.7%, following March’s +2.9%. Excluding gasoline, the headline CPI slowed year over year, to 2.5% in April from 2.8% in March. Canadians continued to battle elevated shelter costs in April (+6.4%), with the largest contributor being mortgage interest costs (+24.5%), notably, mortgage interest rates has been and continues to apply the highest upward pressure on the CPI since December of 2022. The Central Bank sees tightening household discretionary spending as their most viable tool to halt consumer spending on goods and services and attain their 2% inflation target, the CPI dropped below the 3% mark as we predicted in our previous monthly report, we’re expecting further drops until the 2% mark is reached around May, after which the Bank of Canada may need to move quickly to avoid a deflationary scenario, the next slated CPI announcement will be on June 25th.

Job vacancies and Unemployment Rates

The involuntary part-time rate, which comprises of the proportion of part-time workers who could not find a full-time job or who worked part-time due to poor business conditions was 18.2% in May, up from 15.4% observed 12 months earlier.

Job vacancies continued to fall in March, by 40,600 (-6.2%), the biggest month-over-month decline since September 2023. There were 2.2 unemployed persons for every job vacancy in the March, up from 1.9% in the previous month, indicating the labour market tightness has eased, which will continue reduce upward pressure on wage growth.

Bond yields move downwards

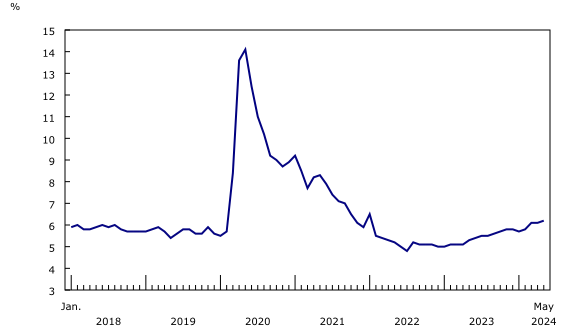

Canada’s 5-year bond yields have continued to move downward since they reached 16-year highs during the month of October. Canada’s mortgage rates tend to track five-year bond yields at a premium and with a lag. Yields dropped due to a growing consensus that interest rates remaining elevated long than anticipated and a hard Canadian recession fear all but diminished as the Canadian economy is now expected to be in a mild recession after a negative Q3 and flat Q4 results.

If you’re looking to buy a home in Canada:

Our current best 5-year fixed rates is 4.70% and 5-year variable rate of 5.85%.

For first-time home buyers, there are some great opportunities, sellers are coming to terms with tapering price growth as higher interest rates have barred many from entering the market, inventory is increasing and will edge up in the middle months of 2024.

For homeowners who are coming up for a mortgage renewal, continue to monitor our rate forecasts, it would be wise to see what rates Perch may be able to offer above and beyond your existing Lender, as they’re typically less aggressive on their rate offerings.

For homeowners who would like to see the benefit of switching lenders and breaking their mortgage early, Perch automatically calculates the net benefit once you input your existing property and mortgage details in your Perch portfolio.