Alex

Alex Est. reading time:

Est. reading time:

Read the 2025 interest rate forecast.

Save money on your mortgage

Don’t leave money on the table

Don’t just go with your bank

Get today’s best rates from our lenders

Key Takeaways

- Our current best 5-year fixed rates is 4.14% and 5-year variable rate of 4.40% (Prime -1.05%).

- For first-time home buyers, there are still great opportunities, sellers are coming to terms with tapering price growth as higher interest rates have barred many from entering the market, inventory is increasing (especially for condos) and should remain at elevated for the next few quarters until more mortgage rate drops prompt sideline buyers to enter the market.

- For homeowners who are coming up for renewal, our Mortgage Renewal Calculator can help you plan ahead to get a sense of what rate you can expect from your lender at renewal, what your new payment would look like and how Perch can help.

- For homeowners who would like to be automatically notified when there’s a benefit to switching lenders and breaking their mortgage early, Perch automatically calculates the net benefit on a weekly basis for all your existing properties. Make sure to sign up for your free profile today.

Mortgage Rates Prediction

For the month of January, we anticipate fixed rates will stay flat and variable rates as well assuming the Bank of Canada holds on January 29th.

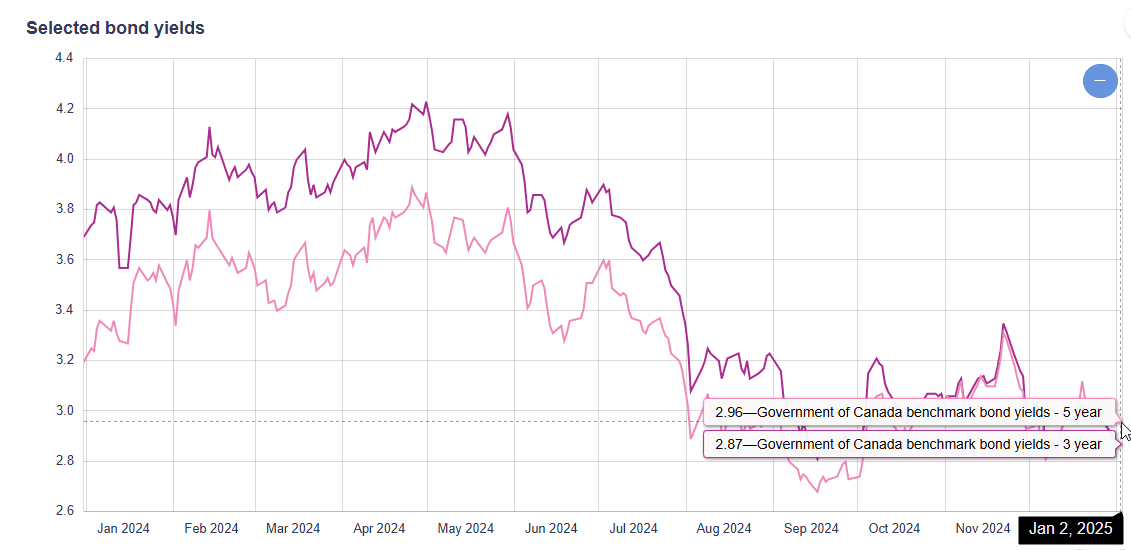

Canada’s bond yields (which influence fixed mortgage rates) have fluctuated, but are largely flat month-over-month (Source: Bank of Canada):

Upcoming Bank of Canada rate announcement (Jan 29, 2025)

We look at some of the core factors that the Bank is monitoring to gauge which direction they are likely to go. In this case, all indicators seem to indicate they will hold.

- Real GDP Growth: The Bank of Canada is expecting GDP growth of 1.2% in 2024 and 2.1% in 2025. This is an acceptable amount of GDP growth and would support a hold. (Source: Bank of Canada)

- Inflation: Core inflation (year over year) in November was 1.6% (vs 1.7% in October), slightly below the Bank’s 2% inflation target and expected to increase in the short-term. (Source: Trading Economics)

- Unemployment: Increased to 6.8% in November (1% higher than 1 year ago). This uptick would potentially justify a cut but the Bank of Canada has hasn’t signalled they think this is an unreasonably high level as it indicates slack in the labour market and wage growth is also reasonable. (Source: Trading Economics)

Buyer Mortgage Balances Prediction: Flat (condos) and up (non-condos)

We believe that non-apartment/condo properties will experience slight upward price movements and apartment/condos prices in major markets will likely face lower prices until excess inventory is absorbed (great to article to read about this for Toronto here).

In addition to this, recent regulatory changes in December 2024 to increase the insured limit from $1M to $1.5M should compound this trend by further reducing demand for condos. Our CEO, Alex Leduc, was recently interviewed in this article on the topic.

Home Prices

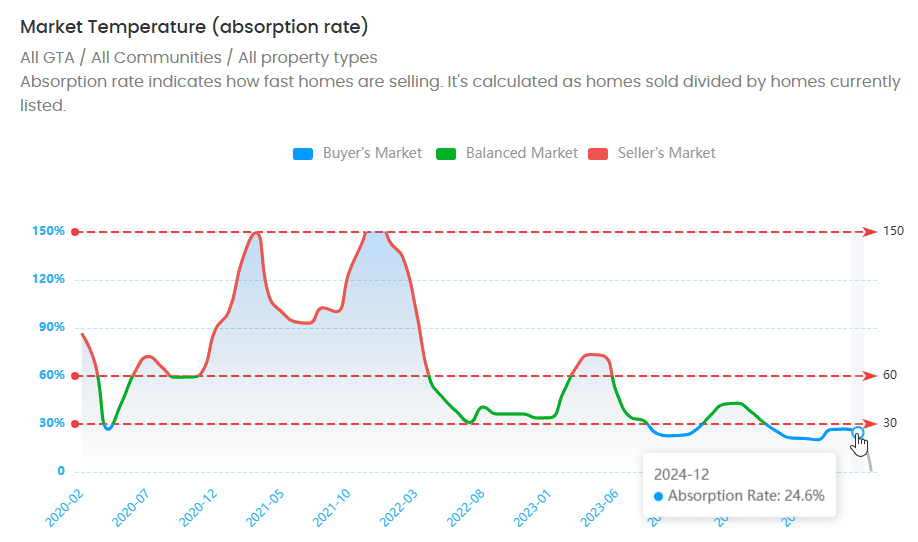

As a general rule of thumb, a sales to new listings ratio (SLR) above 60 is deemed a seller’s market, below 30 a buyer’s market and between the two a balanced market). In a seller’s market, prices are usually rising due to demand outstripping supply avaialble and in a buyer’s market prices are declining due to supply of new listings being greater than the demand from buyers.

Canada as a whole remains a balanced market as shown by CREA below with an SLR of around 59. However, the trend is on the way up into a seller’s market.

This is the national average and some cities have trended well below the average. For example, according to HouseSigma the Greater Toronto Area is a buyer’s market with an SLR of 25.

The SLR for condos is even worse (17), since there has been a flood of new inventory related to new projects hitting the market. Detached homes remain at 28%.

According to CREA, the National Composite MLS Home Price Index (HPI) was up 0.6% between October to November. 2024 overall was fairly flat.