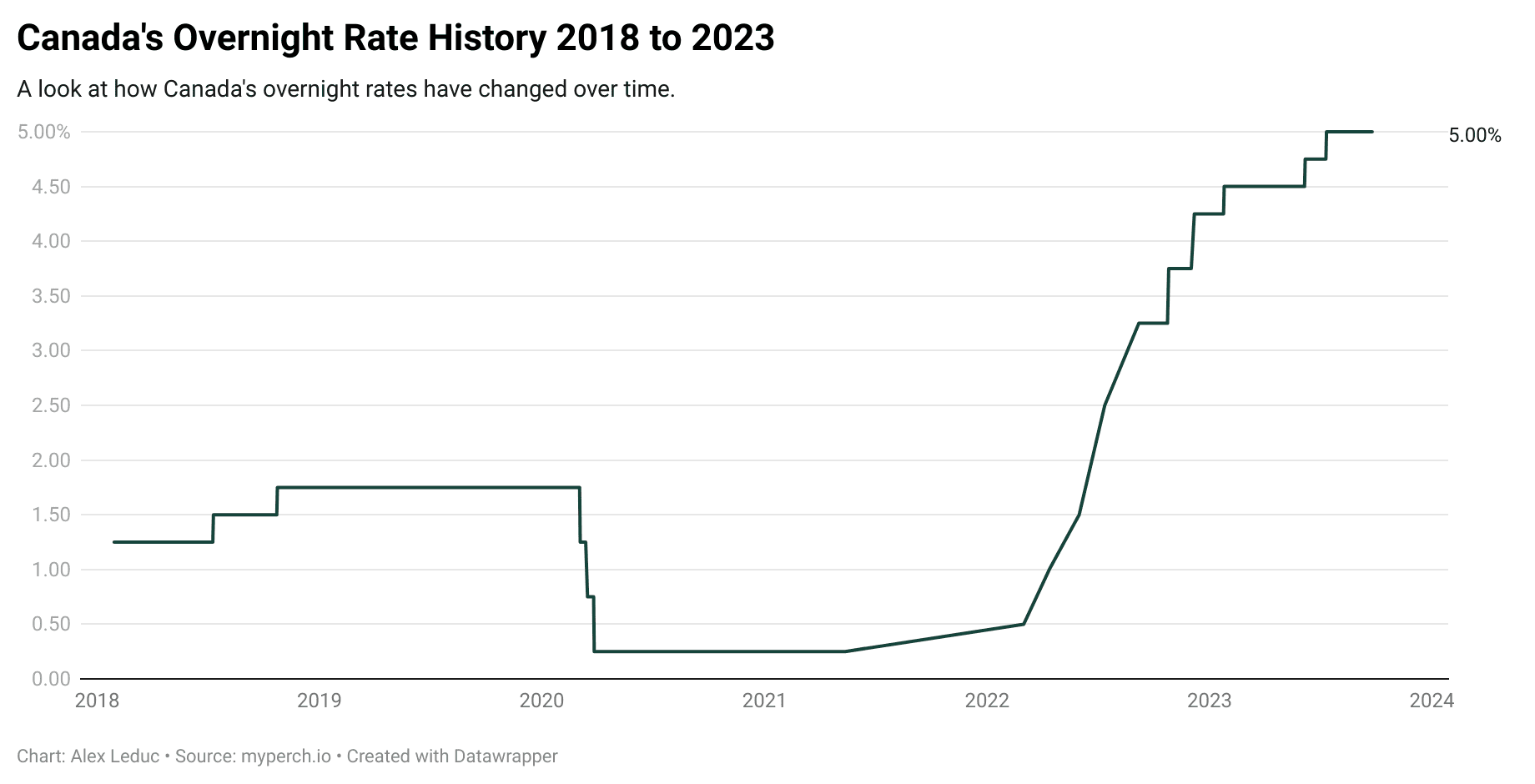

Canada Interest Rate Forecast 2024-2028

Last Updated: December 11, 2024

CURRENT INTEREST RATE FORECAST FOR 2024: 3.25% (last updated December 11, 2024)

Current Forecasts:

For more information about the 2024 Bank of Canada rate announcement schedule, read more here 👈

Key Takeaways (updated December 2024)

- The prime rate in Canada as of December 11, 2024 is 5.95%. (last change: -0.50% on December 11, 2024)

- On Wednesday, December 11, 2024, The Bank of Canada announced that it will be cutting its rate, bringing the policy rate to 3.25%.

- Recent data indicates inflation is decelerating toward the Bank of Canada’s target, coupled with slow economic growth.

2024 Predictions (updated December 2024)

- The Canadian economy continues to show signs of weakness and recent inflation figures hovered at 1.7% last month, below the 2% target. Furthermore, unemployment reached a 3-year record high of 6.8%. This has prompted the Bank of Canada to cut rates further to avoid dragging the Canadian economy down further

Will Interest Rates in Canada Go Down in 2024?

On December 11th, the Bank of Canada cut its interest rate to 3.25%. The next Bank of Canada announcement is scheduled for January 29, 2025.

Commentary from Perch’s CEO and Principal Mortgage Broker, Alex Leduc:

- The Canadian economy continues to show signs of weakness and recent inflation figures hovered at 1.7% last month, below the 2% target. Furthermore, unemployment reached a 3-year record high of 6.8%. This has prompted the Bank of Canada to cut rates further to avoid dragging the Canadian economy down further.

When is the next Bank of Canada rate increase and what can I expect?

The current market overnight interest rate forecast for the remainder of 2024 is:| Variable Rate Interest Forecast 2024 to 2028 (as of December 2024) | |

|---|---|

| Date | 5-year variable rates |

| 11/30/24 |

5.00% |

| 12/31/24 |

4.82% |

| 6/30/25 |

4.48% |

| 12/31/25 |

4.24% |

| 6/30/26 |

4.00% |

| 12/31/26 |

4.26% |

| 6/30/27 |

4.25% |

| 12/31/27 |

4.17% |

| 6/30/28 |

4.25% |

| 12/31/28 |

4.25% |

| 6/30/29 |

4.25% |

| 12/31/29 |

4.25% |

How will the latest Bank of Canada interest rate announcement impact your monthly mortgage payments?

For variable rate mortgages (meaning your payments don’t fluctuate as prime rates change): The October 23rd decrease means that less of your existing mortgage payments go towards the interest portion of your mortgage as your amortization decreases, but your payments will stay the same. Use our Mortgage Renewal Calculator to get an estimation of what your expected rate and payment will be at your maturity date. If the payment isn’t manageable, connect with your advisor well in advance to look at all options.

For adjustable rate mortgages (meaning your payments fluctuate as prime rates change): The latest cut will further decrease your mortgage payments and the outlook shows that further cuts from the Bank of Canada are expected throughout 2024 and into 2025 to further reduce your mortgage payments.

What is the interest rate forecast for 2024 in Canada? (updated December 2024)

Commentary from Alex Leduc, Principal Mortgage Broker and CEO of Perch:

- The Canadian economy continues to show signs of weakness and recent inflation figures hovered at 1.7% last month, below the 2% target. Furthermore, unemployment reached a 3-year record high of 6.8%. This has prompted the Bank of Canada to cut rates further to avoid dragging the Canadian economy down further.

What is CPI and how does it affect the Canada interest rate forecast?

CPI stands for consumer price index and it is the measure of average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. It is mainly used to measure inflation. A rising Consumer Price Index (CPI) would prompt the central bank to raise interest rates. The CPI basket includes 8 main categories of goods and services: Food, Shelter, Household operations, Clothing, Transportation, Health, Recreation, and Alcoholic beverages. CPI data is reported for various geographic areas, including Canada, provinces, and select cities, such as Whitehorse, Yellowknife, and Iqaluit.

What affects the Bank of Canada’s interest rate forecast?

We look at some of the core factors that the Bank is monitoring to gauge which direction they are likely to go. In this case, all indicators justify a cut, which makes it very likely.- GDP Growth: The Bank of Canada is expecting GDP growth of 1.20% for 2024. Q1, Q2 and Q3 2024 came in at 1.8%, 2.1% and 1% respectively, implying a slow Q4 is also expected. (Source: Trading Economics)

- Inflation: Core inflation (year over year) in August ticked up slightly to 1.7% (vs 1.6% in July), now below the Bank’s 2% inflation target. However, with a Trump presidency the risk of higher inflation is now acute. (Source: Trading Economics)

- Unemployment: Holding steady at 6.5% in October (0.8% higher than 1 year ago), the Bank of Canada has signalled they think this is a good level as it indicates slack in the labour market and wage growth is not unreasonably high. (Source: Trading Economics)

What is the Canadian prime rate?

The prime rate is what major banks and financial institutions in Canada use to set interest rates for loans and lines of credit which also include variable rate mortgages.

Is prime rate the same as mortgage rate?

The prime rate is not the same as your mortgage rate. A prime rate is the base cost of borrowing from which lenders start to determine interest rates on mortgages, personal loans, credit loans or other financial products. In general, the prime rate mostly affects variable rate mortgages. Your mortgage rate is the interest rate you are expected to pay on any borrowed money.

What is the mortgage interest rate forecast for 2024 in Canada?

On December 11, the Bank of Canada announced a rate cut, bringing the interest rate to 3.75%.

Our current best 5-year fixed rate is 4.15% and 5-year variable rate is 4.96%.

What are the interest rate predictions from the banks?

CIBC

CIBC Capital Markets views the Bank of Canada’s (BoC) most recent rate cut as expected and aligned with forecasts, bringing the overnight rate to the upper end of the neutral range. With the midpoint of neutral at 2.75%, this move could set the stage for 25 bps cuts in the new year as policymakers assess progress on reducing inflation and stabilizing the economy. Capital Markets anticipates further rate cuts to 2.25% by mid-2025, barring significant fiscal stimulus. They note potential impacts from proposed U.S. tariffs and highlight opportunities for investors in equity and fixed-income markets amid lower rates.

RBC

RBC economists say that “The BoC signaled firmly in December that policymakers are planning a more gradual pace to interest rate cuts going forward, but we continue to expect the overnight rate will ultimately need to fall to net stimulative levels (below the BoC’s current 2.25% to 3.25% estimate of the neutral range) to allow the economy to strengthen and prevent inflation from running significantly below the 2% target”.

Scotiabank

Scotiabank economist say “In Canada, the BoC’s communication signaled a clear guidance of a more gradual easing phase. We expect them to follow December’s 50 bps cut with a 25 bps cut in 2025Q1. This forecast has them holding at 3.0% thereafter until the end of 2026, which is within the upper range of their estimates for the neutral rate. This reflects our assessment of inflation risks in an economy with effectively no excess supply to absorb them”.

TD Canada

TD Economists believe that following a slowdown in 2023-2024, Canada’s economy is projected to rebound to trend growth by 2025-2026, with real GDP stabilizing around 1.9%-2.0% from 2027-2029. Slower population growth will enhance labor productivity, while consumer spending is expected to improve as lower interest rates spur activity. Business and residential investment will benefit from housing demands and clean energy initiatives. Inflation is forecast to stabilize near 2%, allowing the Bank of Canada to cut rates to a neutral 2.25% by 2025. The Canadian dollar is expected to recover to 74-76 U.S. cents as growth aligns with the U.S.

BMO

BMO economists say “with the latest cut, the policy rate hits the top of the neutral range, which the Bank estimates is 2.25%-to-3.25%. That alone could be an occasion for more policy caution, particularly when past easing efforts are already showing some signs of gaining traction (such as in home and vehicle sales). Meantime, there are developments unfolding or looming that could influence economic growth and/or inflation enough to impinge on monetary policy… again, arguing to tread carefully. These include changes to federal immigration policy, changes to federal and provincial fiscal policies (think tax rate holidays and rebate cheques) and the risk of U.S. tariffs.

As before, we expect the Bank’s easing endpoint to be in the bottom half of the neutral range (2.5%, so 75 bps to go). But this could now be a 2025 H2 story with net risks resting on the upside”.

Alex Leduc

Alex Leduc is Founder and CEO at Perch. Prior to starting Perch, he worked in the real estate sector for 8 years in corporate finance, strategy and analytics roles. He is currently a Technical Advisory Committee Member of the Financial Services Regulatory Authority of Ontario (FSRA) and Co-Chair of the Canadian Lenders Association Mortgage Roundtable. Alex is a graduate of Ivey Business School from Western University and a CFA Charterholder. LinkedIn